Last Updated May 13, 2026

It is not uncommon for businesses to struggle while working on net 30 or net 60 payment terms with clients. Since obtaining a loan from banks is not easy for most small business owners, they often turn to invoice factoring.

However, like every other financing option, invoice factoring does not come without a few risks.

Factoring offers clear advantages for business owners, but this article will detail everything B2B business owners need to know about the risks of invoice factoring and how to reduce them.

Why Do Businesses Use Invoice Factoring?

Funding invoices helps businesses build consistent revenue and more predictable cash flow. Plus, factoring companies take charge of handling the invoice collections process for their clients, meaning far less accounting responsibilities.

Companies use invoice factoring for many other reasons, ranging from funding growth to stabilizing seasonal shifts in revenue to covering operating expenses. The complementary credit check that a factor like altLINE performs on new debtor is another lesser-known reason as to why businesses use factoring.

It is a widely used alternative financing solution for small businesses in particular that are looking to expand, as it provides an immediate increase in working capital.

Invoice Factoring Risks

Any financing option comes with its own set of risks. Below is an overview of common concerns you might hear about invoice factoring to help you better understand the potential risks associated with this funding option. Do note, however, that a few of these risks can be alleviated by working hand-in-hand with your factoring company to find solutions to any potential causes of concern.

Loss Of Control Over Invoice Payments

Working with a factoring company relegates control of certain financial aspects of a business to a third party. This is because involving the factoring company to pursue and collect invoices and deficit funds is a loss of privacy for both customers and business owners. This leads to the loss of control over the collections process and invoice payments.

It’s important to note that despite losing control of receivables, this means far less A/R responsibilities fall on your shoulders. The factoring company has professionals to handle collection responsibilities, which is often seen as a positive.

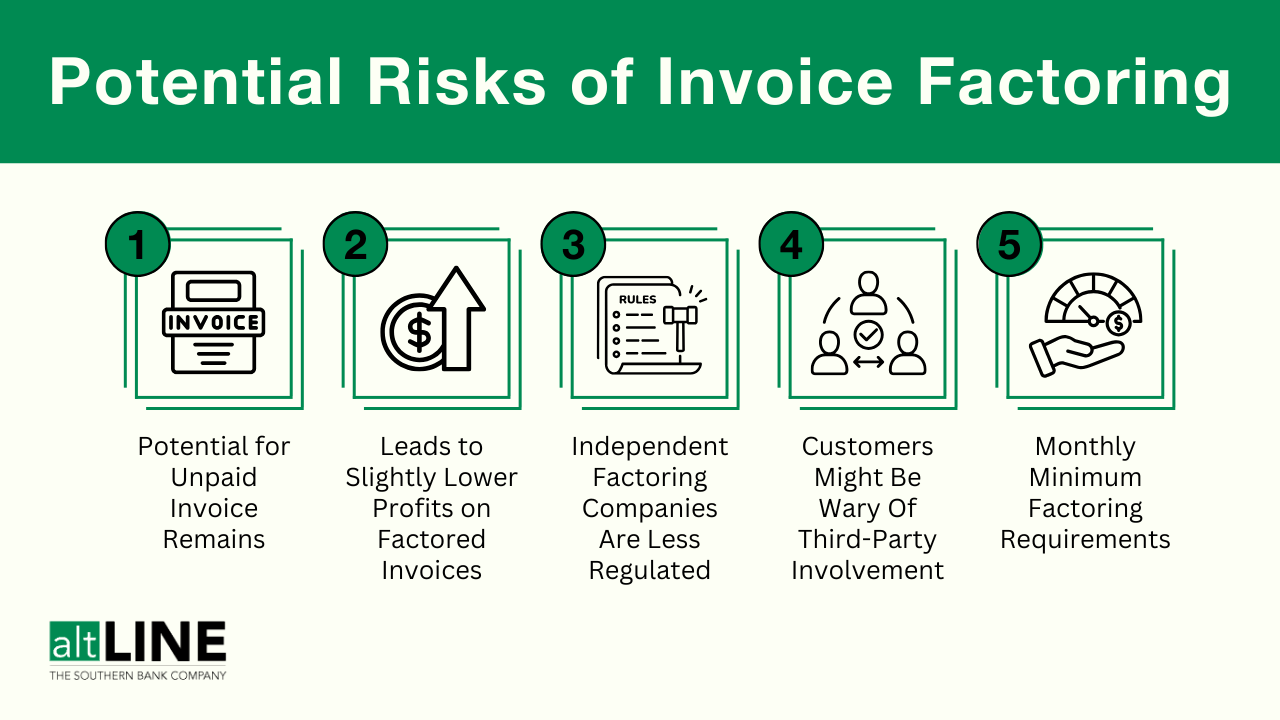

Third-Party Involvement Can Spook Some Customers

Invoice factoring actively involves your business’s customers, so they are fully aware of the transfer of the invoice rights and payment process. Though most debtors are familiar with factoring and know that it is legitimate, this process change could cause friction in the customer-business relationship if not communicated effectively.

This is why altLINE has an account manager dedicated to the customer onboarding process, ensuring your customer relationship remains in good standing as you begin the factoring process.

Potential For Unpaid Customer Invoices Remains

There are two types of invoice factoring: recourse vs. non-recourse factoring. Some business owners may see recourse factoring as a risk, because under this type of agreement, businesses are still required to chase the payments of unpaid invoices if their customers refuse to pay. With recourse factoring, the business buys back the unpaid invoice if the factoring company cannot collect payment on it – they are held liable for non-payment.

However, this risk of non-payment by customers is not typically an issue if your customers reliably make invoice payments. Also note that recourse factoring provides certain benefits, such as lower cost and a faster approval process than non-recourse factoring.

Slightly Lower Profit Margins

Invoice factoring fees are typically 1-5% of the total invoice value, which is usually a bit more expensive than other forms of financing. These higher fees can lead to a lower profit margin for businesses. For instance, if an invoice of $5,000 is sold with a 3% factoring fee, the business owner receives $4,850, resulting in a lower profit with the $150 loss.

While invoice factoring tends to be more expensive than more traditional forms of financing, it is easier to qualify for, which could make it a good fit for your business. Plus, it takes a significant amount of work off your plate.

Long Contract Terms

Many factoring companies require long contract terms that might span at least one year, which can prevent business owners from easily pulling out of the agreement. If you are looking for a solution to improve cash flow for your small business, it may be difficult to cope with the long duration of a factoring agreement.

The standard factoring contract is typically 12 months, with a window of notification toward the end to opt-out of renewal for no charge.

Minimum Factoring Requirements

Some factoring companies require clients to factor a certain number of invoices per month at a certain value for an agreement to be reached. This can be challenging for small business owners who are just starting or do not yet have a well-defined, loyal client base. If you are concerned about having a minimum factoring requirement in your contract, you can try to negotiate it out prior to signing. These types of contract terms tend to be flexible and negotiable.

Interest Rates and Additional Charges

There’s also the risk of shady providers including hidden charges and fees, resulting in this type of financing option becoming more expensive.

Keep an eye out for additional charges in the contract, such as origination fees, monthly access fees, lockbox fees, and credit approvals. Many of these charges can be negotiated out of a factoring agreement prior to signing, although some of them will be required no matter the factoring company.

An honest factoring company will be upfront about the total cost of factoring. According to altLINE VP of Operations Kelley Burnett, there are some cases where a slightly different form of factoring might make sense.

“If you’re trying to factor dozens or hundreds of small invoices rather than a more select few large invoices, it can become super arduous and more costly,” Burnett said. “In these cases, we’ll suggest a bulk A/R transaction, or ledgered line of credit. Rather than buying 10 individual invoices, we’ll buy the entire book of receivables and advance the majority up front.”

Regardless, factoring companies should do their best to be a bit flexible to work with you to ensure you’re getting the most out of the transaction.

Client Restrictions

Working with a factoring company incorporates the factor into the day-to-day operations of a business, and as such, they can have influence over which client invoices are factored.

Many factoring companies will not factor invoices for customers that are not creditworthy or reliable. This is because they have to protect themselves from non-payment.

Burnett adds that it’s important to remember that factoring companies are married to your success once an agreement begins. It’s important to be careful with who you choose to do business with.

“Your potential customer could be a terrible payer, either one foot in bankruptcy or just shopping for suckers,” Burnett added. “Our complementary credit checks are a value-added service to you. Sometimes it’s better to walk away than to do all the work and never get paid. That’s a way to go out of business really fast.”

However, if your customers consistently make on-time payments, this should not be an issue for your business.

How to Mitigate Invoice Factoring Risks

To reduce the risks listed above, it is ideal to use a trustworthy and reliable factoring company so that you and your customers can feel secure in the factoring relationship. Independent factoring companies are largely unregulated, which can make the risks outlined in this article more worrisome if you choose the wrong factoring company. We recommend doing thorough research and vetting of your factoring company prior to signing a contract with them.

altLINE is a unique factoring company because it is a division of the Southern Bank Company. Working with a bank factoring company that’s FDIC insured and state regulated, ensures there’s maximum transparency between the factor and you.

To work with an invoice factoring company that has 90+ years of experience serving customers, you can get a free quote or give altLINE a call at +1 (205) 607-0811. We would love to help you get started on an easy funding journey.