Last Updated January 22, 2026

Invoice factoring has become an extremely popular financing tool for small, growing, and new businesses to keep cash flow steady. But like any funding solution, factoring comes with its pros and cons.

Before partnering with a factoring company, you’ll want to know what you’re getting into. While factoring is generally considered low risk compared to other forms of financing, it’s not necessarily zero risk.

In this guide, we’ll break down all of the advantages and disadvantages of factoring, so you feel confident you’re making the right decision when deciding whether or not to factor your invoices.

How Does Invoice Factoring Work?

Invoice factoring is the process of selling unpaid client invoices to a factoring company in exchange for an immediate cash advance.

Factoring can be explained in a few simple steps:

1. A business reaches a deal with a third-party factoring company (known as a “factor”) to sell existing and future outstanding accounts receivable to the factor.

2. Once the business invoices their customer, the business sends a copy of the invoice to their factoring company and is immediately advanced 80-90% of the value of the invoice.

3. The factoring company assumes collection responsibility on the invoice.

4. The customer submits payment to the factoring company.

5. Once payment is received and processed, the factor releases the remaining value of the invoice to the business, minus a small factoring fee (0.75-3.50%).

Most companies factor receivables due to long payment terms or slow-paying customers, disrupting cash flow. However, some businesses with reliable customers or normal payment terms still choose to factor their receivables to increase working capital, since it’s a low-risk form of financing.

What Are the Advantages of Factoring?

Whether you’re a new small business owner or you manage an established company, factoring invoices can be a major asset for your B2B strategy. It offers benefits that other traditional lending options can’t provide, plus it is a more accessible solution for many businesses.

Below are some of the biggest advantages of factoring for B2B businesses.

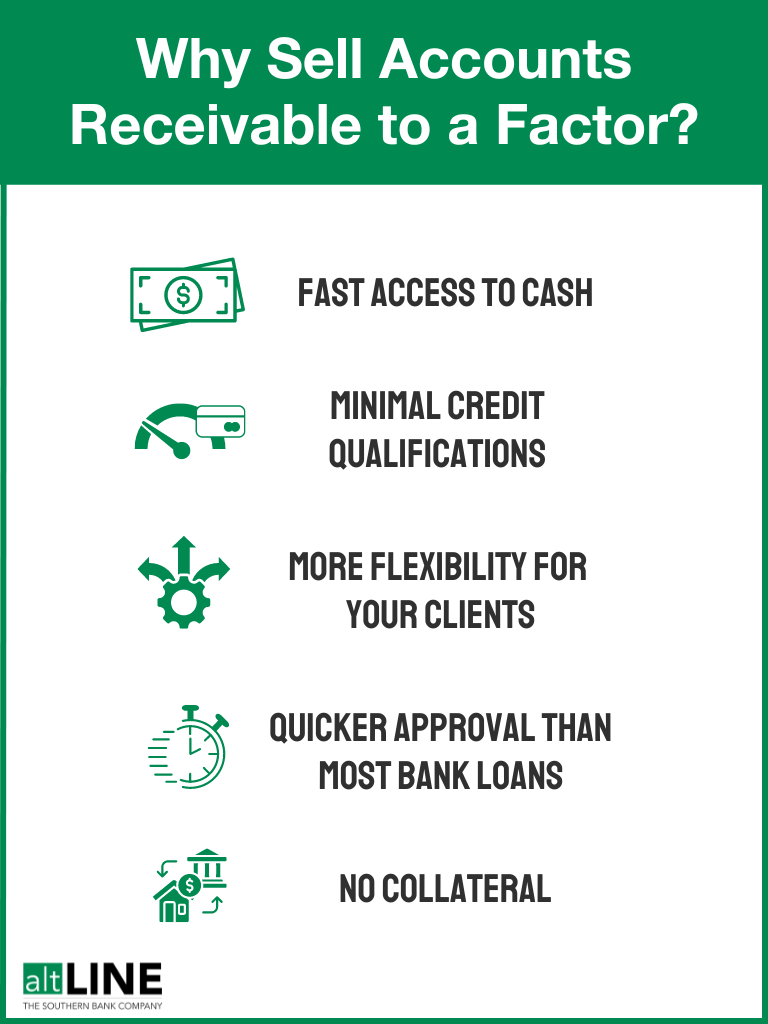

Quick Cash for Your Business

Perhaps the most obvious reason why businesses turn to invoice factoring: it provides fast cash to keep processes running smoothly.

With invoice factoring, you receive a cash advance, while other alternative financing options provides a loan that you must repay.

There are legitimate reasons why a business owner would need to get access to the fast cash, such as:

- Paying employees

- Settling monthly bills

- Bringing in fresh inventory

- Expanding to a new location

- Helping manage overdrafts

Factoring is often used by businesses in industries with notoriously thin margins, such as trucking, though businesses across all industries reap the benefits.

Easier Approval Than a Traditional Loan

Getting a loan can prove out-of-reach for businesses with limited collateral and a short financial history. However, invoice factoring companies pay the most attention to the credit scores of your customers. That means a faulty or nonexistent track record won’t matter as much when you apply.

According to altLINE Vice President of Operations Kelley Burnett, this is one of the most common reasons small business owners choose invoice factoring.

“Factoring offers an unprecedented opportunity to start or grow an existing business by focusing more on the creditworthiness of a client’s customer base,” Burnett said. “A factor knows that invoices purchased from strong, creditworthy customers will be paid back. A factoring facility relies on the strength of a client’s accounts to enable growth. This way, the only thing standing in the way of growing your business, is your ability to solicit and service new, creditworthy customers.”

The fact that almost any business can qualify for factoring, regardless of credit history, is a huge advantage of factoring for startups and small businesses.

More Flexibility for Your Clients

Increased cash flow for your company means you can allow customers more leeway when it comes to working out payment terms. Instead of requiring immediate payment, you can give clients a month or more to complete the invoice, without worrying about the strain it’ll place on your own business. And if you’re already working on extended payment terms, you won’t have to rely on debtor payment habits to dictate your cash flow.

Limited Risk for Your Business

Unlike a traditional loan, which requires collateral, invoice factoring is unsecured. Therefore, you won’t need to worry about valuable assets being seized if the customer fails to pay.

If the customer does fail to pay, a good factoring company will work with you to find a fair and sensible solution.

Another example of how factoring reduces risk is the fact that a reputable factoring company like altLINE provides complementary credit checks for your existing and potential new customers. Many users, including small business owner Krissy Wellman, testify that this is actually the biggest benefit of factoring.

“The thing I like the most is that you credit check our potential clients before we start doing real business with them,” said Wellman, CEO of Wellman’s Staffing. “We absolutely love that you’ve helped us figure which businesses we can do business with and which businesses to avoid partnering with.”

Highly Accessible Funds

After you initially set up an account with an invoice factoring company, you should be able to receive cash within 24 hours of submitting an invoice. Some factoring companies, including altLINE, have online portals to make it easy to track progress.

What Are the Disadvantages of Factoring?

Factoring isn’t always the best option for every business. Be sure to weigh the potential drawbacks of factoring before determining what’s best for your business.

Here are some of the potential disadvantages of invoice factoring:

Negative Stigma Around Factoring

While invoice factoring is, at its core, a business practice like any other, some might find that it has a dark past. Certain lenders have been known to take advantage of clients with confusing language and dodgy practices, though industry standards have since evolved for more transparent transactions.

Slightly Reduced Profit Margins

The factor company basically takes a cut out of each invoice. Even though it can be as low as 1-3%, you’re still losing a bit of income in the long run which may affect your company’s monthly budget.

However, according to altLINE VP of Operations Kelley Burnett, the amount of back office work a factoring company can do for businesses can make up for the slightly reduced profit margins.

“Some users are really cost-conscious once they figure out how much it costs,” Burnett said. “But we’re also managing their receivables. We have a whole staff that’s calling their customers, verifying invoices, vetting new customers—there is a lot more labor on our end that benefits their company. Most consider this to make up for any lost dollars.”

Collection Still Isn’t Guaranteed

Just because the factoring company buys the invoice doesn’t mean the customer is guaranteed to pay. In some cases, you might be required to settle the bill if the invoice isn’t cleared. However, if you’re using non-recourse factoring, you won’t be responsible for any missed company payments; rather, the factoring company will accept responsibility.

Hidden Costs and Fees from Non-Bank-Affiliated Providers

Even if you’re OK with the quoted factoring rate, be wary of additional costs and be sure to conduct thorough research before signing on. Make sure to read the fine print and ask questions up front.

Note that not all factoring companies are the same. There are two types of factors: bank-affiliated factoring companies and independent companies.

It’s best to prioritize bank factoring companies when searching for a provider, as they are federally regulated and pull funds from their own pockets, rather than unknown third parties. Independent companies pose much more risk.

In Summary: Advantages vs. Disadvantages of Factoring

Factoring is a very accessible alternative financing option with much easier approval than those bank loans.

With that being said, here’s an overview of all of the advantages and disadvantages associated with factoring:

| Advantages of Factoring | Disadvantages of Factoring |

| Reliable access to quick cash | Potential for slightly reduced profit margins (typically 1-5% factoring fee) |

| Easier approval than most traditional bank loans, including for businesses with low credit or lack of credit history | Stigma surrounding invoice factoring or related alternative financing methods |

| Added flexibility for client payment terms | Certain independent factoring providers can add hidden costs and fees, requiring need for due diligence related to finding a truthful provider |

| Limited risk for your business compared to most traditional financing methods | Collection isn’t guaranteed (when using non-recourse factoring) |

| Highly accessible – most factoring companies allow business owners to manage entire process online | Certain factoring providers can add hidden costs and fees, requiring need for due diligence related to finding a truthful provider |

Like any business practice, invoice factoring comes with pros and cons. Carefully consider the ‘why’ behind your choice. Will it help your company grow and expand? Are you planning on investing the money back into your merchandise or employees?

If your answer is yes, the advantages of factoring likely outweigh the disadvantages. If you’re interested in learning how factoring can benefit your business, request your free factoring quote from altLINE.

Advantages and Disadvantages of Factoring FAQs

Below are some of the most commonly asked questions about factoring your accounts receivable.

What is the main advantage of factoring?

Invoice factoring has several advantages, but the main advantage of factoring is the immediate cash flow boost it provides a business. Unlike many financing options, factoring does not require the borrowing business to tie collateral to the funds. For many business owners, this is the most enticing aspect of invoice factoring.

How much do factoring companies charge?

Generally, a factoring company will charge 1-5% (this is considered the “factoring fee”) of the total invoice value, depending on variables such as your factoring volume, invoice size, risk profile, and client credit. If your company factors many invoices and works with trustworthy clients, your fees will generally be lower.

What type of business typically utilizes invoice factoring?

At altLINE, we encourage small to medium-sized businesses to look into invoice factoring, as typically these are the businesses that would benefit most from quick cash flow boosts. It’s important to explore and weigh your options, so if you’re a business owner with questions about the factoring process, feel free to give altLINE a call at +1 (205) 607-0811.

Grey was previously the Director of Marketing for altLINE by The Southern Bank. With 10 years’ experience in digital marketing, content creation and small business operations, he helped businesses find the information they needed to make informed decisions about invoice factoring and A/R financing.