Last Updated December 1, 2025

Plenty of businesses face funding challenges. Whether you just need enough to make payroll or you want funding to grow your business, there are plenty of options to get the cash you need.

Most lending options fall into one of two categories: asset-backed loans and cash flow-based loans. Each loan type comes with different requirements and considerations and understanding how they differ could make all the difference in how you grow your business.

In this guide, we’ll break down the key differences between an asset-backed loan vs. cash flow loan, explore real-world examples of lending for businesses, and help you weigh the pros and cons of each option. Whether you’re considering a cash flow-based loan, working with a cash flow lending corporation, or just comparing cash flow vs. asset-based lending options, this guide will provide you with the clarity you need to make the right decision.

What Is Cash Flow Lending?

With cash flow lending, lenders provide funding based on your business’s projected future cash flow rather than its current assets. In this financing model, your ability to repay the loan is tied to the income you expect to generate. This makes cash flow-based lending ideal for businesses with strong, predictable revenue but limited physical collateral. This type of lending isn’t right for all businesses, but it can improve cash flow during times of growth if you have otherwise predictable income.

Unlike asset-based loans, which require you to pledge physical assets like inventory, equipment, or real estate as collateral, cash flow-based loans rely on EBITDA (earnings before interest, taxes, depreciation, and amortization), historical financial performance, and growth potential to determine your creditworthiness.

Examples of Cash Flow-Based Loans

There are several types of cash flow-based loans. Some of the most common include:

- Term loans: Many cash flow lending banks offer medium to long-term loans with fixed repayment schedules. These loans are based on your income projections and financial statements, rather than collateral.

- Unsecured lines of credit: A revolving credit line allows businesses to draw funds as needed.

- Merchant cash advances (MCAs): Although they’re expensive, MCAs are an alternative that provides upfront capital in exchange for a portion of future revenue. They’re a high-risk form of cash flow lending for businesses, though, with daily or weekly repayment terms based on sales volume.

- Revenue-based financing: This type of cash flow-based loan allows companies to repay a percentage of their monthly revenue until the loan is paid back. It’s especially popular with SaaS and subscription-model businesses that generate consistent recurring income.

What Is Asset-Based Lending?

With asset-based lending, you secure a loan with tangible assets. Unlike cash flow-based lending, where approval hinges on your projected earnings, asset-based loans are tied to collateral like inventory, accounts receivable, equipment, or real estate.

Asset-based lenders evaluate the value and liquidity of your assets to determine how much credit to extend. If you default on payments, the lender can seize and sell the collateral. This structure makes asset-based loans a lower-risk option for lenders, although there is the risk that you’ll lose your collateral. Still, asset-based lending is more accessible to companies with physical assets but weaker cash flow, which can help bridge funding gaps and keep your business afloat.

Examples of Asset-Backed Loans

There are several types of asset-based loans, including:

- Accounts receivable financing: With accounts receivable financing, you can unlock cash tied up in unpaid invoices without waiting for customers to pay. And if you’re looking for a similar but option that doesn’t actually incur debt, you can explore invoice factoring.

- Inventory financing: Inventory financing is a popular asset-based loan for wholesalers, manufacturers, and retailers, where they can use unsold inventory as collateral to borrow working capital.

- Equipment loans: Companies can leverage machinery, vehicles, or tools to secure funding. This type of lending is useful for capital-intensive industries like construction or logistics.

- Real estate secured loans: You can pledge commercial real estate to access large loan amounts at lower interest rates. It’s a classic example of asset-backed lending for businesses with valuable property holdings.

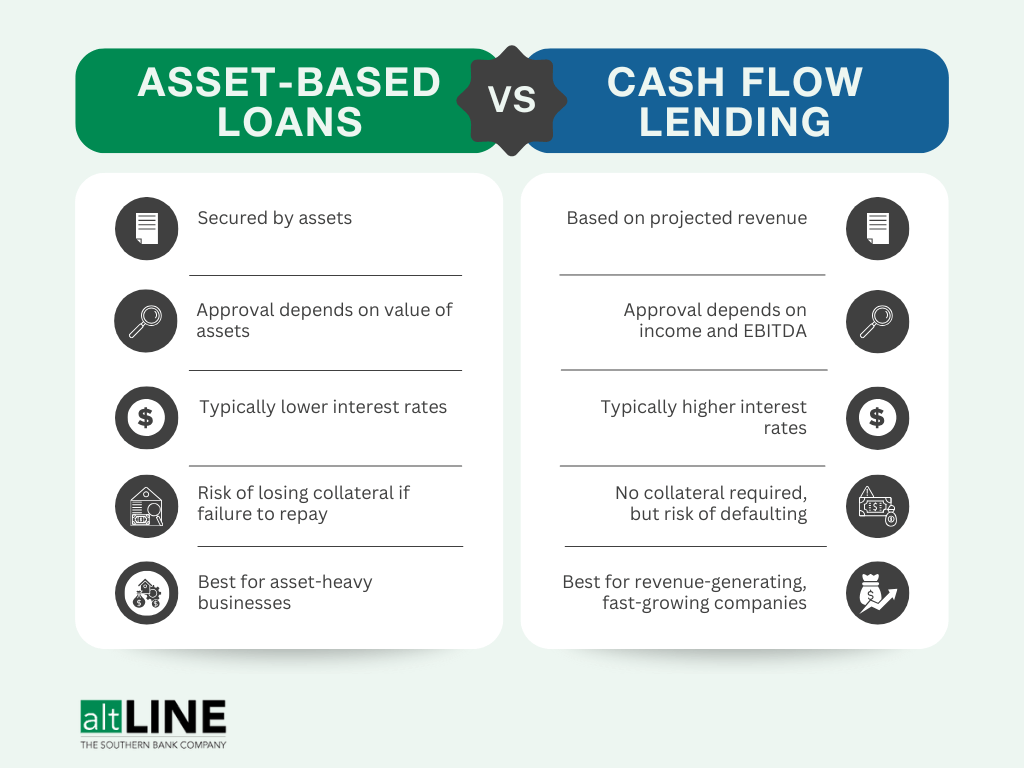

Differences Between Asset-Backed Lending vs. Cash Flow Loans

While both financing options help your business access capital, the key difference between an asset-backed loan vs. cash flow loan lies in how the lender approves and secures your loan.

| Asset-Backed Lending | Cash Flow Lending |

| Relies on physical assets like inventory, receivables, or equipment | Relies on projected income and EBITDA |

| Must commit tangible assets | Unsecured loan based on potential earnings, not assets |

| Ideal for asset-heavy businesses | Ideal for revenue-generating companies with strong income but few assets |

| Risk of losing assets if loan isn’t repaid | Risk of high interest rates and defaulting if cash flow becomes inconsistent |

Asset-Backed Loan or Cash Flow Loan: Which Fits Your Business?

Both types of financing can be valuable tools, but they serve different needs and risk profiles. It’s important to pick the right option, given your decision can play a significant factor in your small business’s growth.

If your company has significant physical assets—such as inventory, equipment, or real estate—an asset-based loan could be a better fit. This type of loan allows you to unlock the value of what you already own. It’s especially popular in industries like manufacturing, retail, and transportation, where tangible assets are abundant and have stable value.

Since the loan is secured, you may be eligible for lower interest rates and more favorable terms. However, lenders will often closely monitor asset value, and failing to meet repayment terms could result in the forfeiture of collateral.

On the other hand, if your business is growing quickly, has consistent revenue, and minimal physical assets, a cash flow-based loan might make more sense. Cash flow-based lending is ideal for service companies, tech startups, or consulting firms that rely more on people and processes than on physical inventory.

In this case, lenders determine your ability to borrow by your income and EBITDA, rather than your balance sheet. While cash flow lending for businesses typically comes with higher interest rates, the streamlined process and lack of collateral requirements can be faster and more flexible.

In-Summary: Asset-Backed Lending vs. Cash Flow Lending

Whether you’re working with a cash flow lending corporation, evaluating offers from cash flow lending banks, or simply comparing cash flow vs. asset-based lending, your choice should align with how your business operates and where you want it to go.

There’s no one-size-fits-all solution to cash flow gaps. But with the right insights and a solid grasp of both cash flow-based loans and asset-based lending, you’ll be better equipped to choose the best funding option for your goals.

Michael McCareins is the Content Marketing Associate at altLINE, where he is dedicated to creating and managing optimal content for readers. Following a brief career in media relations, Michael has discovered a passion for content marketing through developing unique, informative content to help audiences better understand ideas and topics such as invoice factoring and A/R financing.