Last Updated September 24, 2025

It’s one of the most worrisome questions for employees and business leaders alike: what happens if a company can’t make payroll?

Figuring out how to pay employees on-time should be a top priority. Not paying your employees on-time can have disastrous consequences for your business. And even if you have good intentions, this can still be difficult. Processing payroll takes up to five hours for the average small business owner, which is a long time considering all the other tasks you’re likely juggling.

With that said, this guide is aimed to help small business owners find a viable solution for not having the money to pay employees. While not ideal, there are a few methods to look into that can help mitigate the impacts of missing payroll.

What Happens If a Company Can’t Make Payroll On-Time?

A recent report revealed that nearly half of all employees (49%) would leave a company if they were either paid late, not paid at all, or received an incorrect paycheck.

Employees expect to be paid for the work they’ve done for a company. When they were hired, you likely outlined pay expectations in accordance with local payday regulations, such as providing payments every two weeks or twice per month.

When a company cannot pay employees on-time, a significant promise has been broken, and trust is lost. The financial pressure that they experience from late payments will likely cause workers to seek employment elsewhere.

When companies miss payroll, consequences can be even more far-reaching and potentially devastating. Failure to pay wages or remit payroll taxes over an extended period of time can also result in fines and other legal action. Unpaid payroll tax penalties can be assessed on top of the deposits you already owe, further adding to your financial struggles. And disgruntled employees could file a legal claim for their unpaid wages. They will often need to be paid interest and an additional penalty payment on top of their regular paycheck that wasn’t paid on-time.

Poor employee retention can further increase costs for your business through lost productivity and the expenses associated with hiring and training a replacement. High turnover can also hurt your workplace culture, making it even harder to attract and retain top talent.

If your company has no money to pay employees, things can snowball into even more severe outcomes for your business.

Common Reasons Companies Can’t Make Payroll

Not being able to make payroll often comes down to cash flow problems. There are several common cash flow issues that leave companies with no money to pay employees.

Delayed Customer Payments

For example, delayed customer payments can put significant strain on a business’s financial situation, even when they are managing their finances wisely. Other factors outside of a business’s control could include increases in material costs or inventory obsolescence. Increased expenses or reduced income can make it much harder to make payroll.

Investments in New Products or Projects

Of course, a business’s own activities can also make payroll a challenge. New projects and products that require substantial investments can create problems if you don’t have a financial safety net in place — especially if these projects experience delays or other cost-related issues.

Cash Flow Fluctuations

Seasonal businesses can also have a harder time making payroll, as periods of large cash inflows and outflows followed by periods of minimal business activity can make it harder to manage capital effectively. This could even result in periods of negative cash flow during the off-season.

Ultimately, finding ways to improve cash flow is essential so that payroll struggles don’t become a recurring problem for your business.

What to Do If You Can’t Make Payroll

The first step should be understanding what caused your company to miss payroll. This will allow you to make the necessary changes to your processes moving forward to ensure it doesn’t happen again.

Then, you should be transparent with your employees about dropping the ball. Don’t make excuses but be as open and honest as possible and ensure them that you’ll be doing everything in your power to make it up to them. Remember that the human element is of utmost importance. You want to do your best to maintain a decent relationship with your employees. While there’s a good chance that they’re going to lose some of their faith in you in the interim, stress that you are going to work tirelessly to make payroll process improvements moving forward. Be transparent with what changes you’re going to make to make sure they’re paid on-time in the future.

Finally, get to implementing those changes. Whether it’s using payroll funding, enforcing late payment fees with debtors, or lengthening terms with your suppliers, all of which we’ll touch on later in this article, it’s critical to have a plan of action.

How to Make Payroll On-Time

If you’re worried about how to get money for payroll, you have several solutions available. Even when cash flow trouble exists, proactive planning will ensure you can make payments on-time.

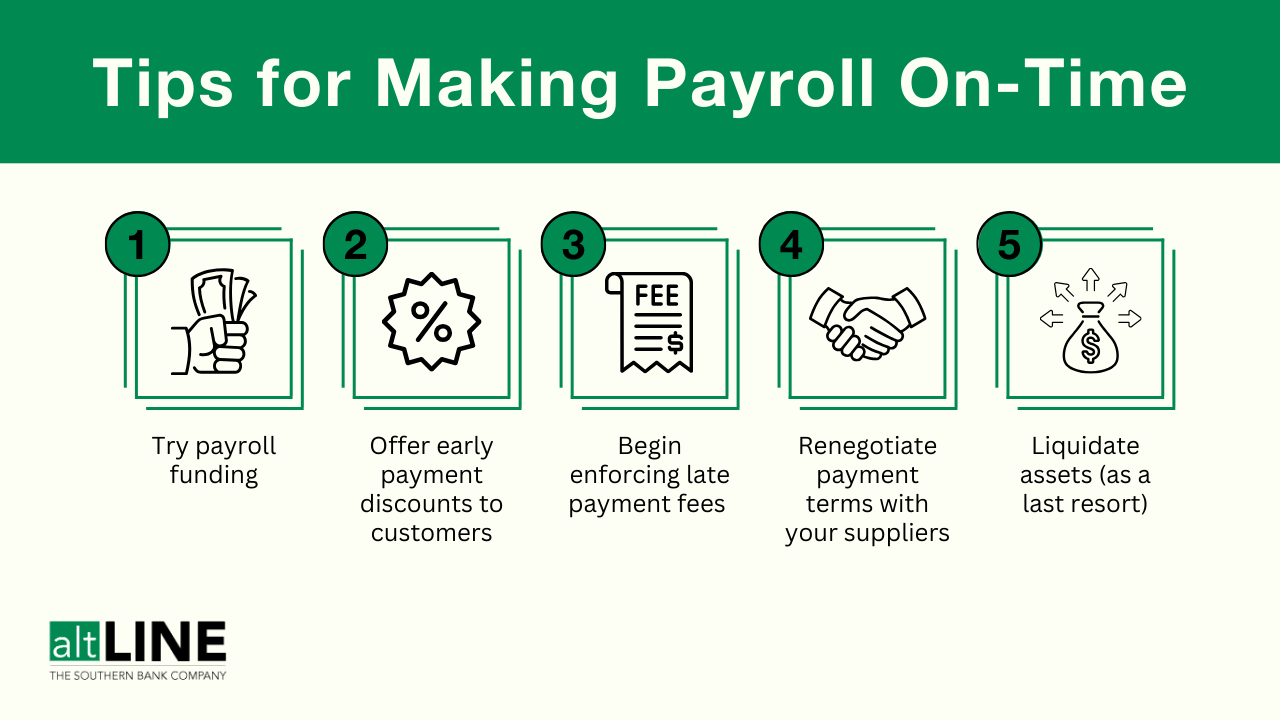

1. Use Invoice Factoring (Also Known as Payroll Funding)

Invoice factoring, also referred to as payroll funding when utilized by staffing companies or freight factoring when utilized by trucking companie, is an excellent solution for paying employees when you are low on working capital. With this solution, businesses sell outstanding invoices to an invoice factoring company, who immediately advances 80% to 90% of the invoice’s value to the business.

When the debtor is ready to pay, they submit their payment to the factoring company, rather than your business. Once that payment is made, the factoring company releases the remaining value of the invoice to your business, minus a small “factoring fee” (typically 0.75-3.50% of each invoice value).

With payroll funding, you get instant cash without taking on additional debt or having to wait for slow-paying customers. Additionally, approval tends to be much easier than trying to take out a bank loan. This can provide a sudden influx of cash without needing to hunt down client payments or add to your list of liabilities.

2. Apply for Payroll Loans

Payroll loans are typically provided to businesses as either a cash advance or a line of credit. With a cash advance, businesses are provided a lump sum of money upfront, which they can use to cover payroll and other necessary expenses. The business must then repay those funds (with interest) by an agreed-upon date. These loans usually feature fixed payments, allowing businesses to plan for them as part of their monthly budget.

A business line of credit operates similar to a credit card. Businesses can borrow money up to a set amount and make repayments (once again, with interest) to lower their balances. With a line of credit, you can withdraw and pay back money multiple times, as long as you don’t reach the limit of your available credit.

Both of these payroll loan solutions can help businesses cover payroll expenses with relatively quick access to cash. Unlike with invoice factoring, these loans enable businesses to keep 100% of the revenue they are owed from unfilled invoices.

However, the loan approval process tends to take longer than payroll funding. Plus, qualifying usually requires a strong credit score, also unlike payroll funding. These loans often have strict repayment requirements and high interest rates, too. Therefore, the long-term costs associated with payroll loans can end up much higher than revenue reductions from payroll funding.

3. Offer Early Payment Discounts to Customers

Some companies will offer early payment discounts to their clients to convince them to submit payments promptly. A common example is 2/10 net 30. With this early payment discount, debtors get a 2% discount if they pay within 10 days of a net 30 payment cycle. Another example is 1/10 net 30, where debtors get a 1% discount, or 2/10 net 60, where they get a 2% discount for paying within 10 days of a net 60 cycle.

These initiatives can encourage buyers to pay quickly to save a bit of cash, thus benefitting both parties. Plus, it can improve your working relationship with your customers.

4. Begin Enforcing Late Fees

Late payment fees can also encourage clients to pay on-time, thus boosting your immediate working capital. Nobody wants to be hit with late payment penalties. Plus, if a customer is struggling to come up with the funds to pay by the due date, knowing that a late fee is in place can encourage them to be transparent and open a line of communication with you to try to work out a sensible solution.

It’s important to do your research on late fees to ensure you’re enforcing a fair system that is stringent enough to nudge buyers to abide by terms, but not too strict so that the fees are higher than what laws might allow.

5. Reevaluate Payment Terms With Suppliers

You can’t delay payroll — but you may have some room to negotiate on your current accounts payable. You might need to wait until the end of the payment term deadline to submit a payment to a vendor. Or, you might need to reach out to a vendor to negotiate a longer payment term. Waiting to fulfill accounts payable instead of paying a vendor right away could help you make payroll as it would allow you to have cash available for a longer period of time.

With cash flow forecasting, you can better evaluate how accounts payable relates to your payroll responsibilities. Combining this information with estimated incoming payments will help you plan and budget appropriately.

6. Liquidate Assets

Though this may come across as a more extreme solution, businesses can liquidate some of their assets to get cash so that they can make payroll. Generally speaking, this could include assets that are no longer used or wouldn’t disrupt your core business operations if sold, including raw materials, existing inventory, and even office equipment, machinery, or manufacturing supplies.

Businesses must be careful to not liquidate more assets than necessary, as this could make it harder for the business to operate. This should be seen as a last resort.

In-Summary: Missing Payroll

Even the most successful, hard-working business owners can be confronted with the possibility of missing payroll. Sales could unexpectedly slow down, the economy might worsen, or you could be faced with a completely unavoidable financial hurdle, such as customers failing to pay for your services.

But workers won’t care what the reasons are and if their employee’s intentions are in the right place. When a company cannot pay its employees on-time, it can be detrimental to their personal financial situation.

Thankfully, there are a few solutions that can throw you a life raft. One of these in particular, invoice factoring, is tailormade for payroll challenges where businesses are short on immediate working capital and need a quick cash flow boost.

Need Cash Fast to Make Payroll On-Time? Consider Invoice Factoring with altLINE

One of the most common reasons companies struggle to make payroll occurs when debtors fail to abide by payment terms or wait until the last minute to pay for your services. If you’re working on net terms with your customers, invoice factoring can be a perfect solution to accelerate cash flow.

Once you invoice a customer, a factoring company such as altLINE will advance the majority of the value of each invoice (up to 90% or more) within 24 hours, allowing you to free up cash and pay your own employees. Factoring is commonly used by small businesses because it’s much easier to qualify for than a traditional bank loan and the application process is quicker and involves less documentation that most forms of financing. Plus, you won’t incur debt as it’s not technically a loan-a factoring company is literally purchasing your invoices at a discounted rate.

If you believe you are a good fit, fill out our free factoring quote form. Or, if you have any questions about the process and would like to speak with a representative, give us a call at (205) 607-0811. We are happy to help!

Missing Payroll FAQs

Is it illegal to pay employees cash?

You can still pay your employees in cash, as long as you still comply with IRS requirements and take out appropriate deductions for each employee. To legally pay employees in cash, you must keep detailed payment records, follow a regular payment schedule to ensure accurate payments and stay compliant with state payday laws, and pay all applicable taxes. You should also get an acknowledgement of the cash payment from your employee (such as by having them sign a salary receipt).

Is it illegal not to pay employees?

Yes. Employers are not allowed to withhold or deduct payments from their employees, except in situations required by law (such as FICA taxes or wage garnishment). This is true even if the company is experiencing cash flow problems. Failure to pay employees is considered wage theft. Employees can sue for compensation, and businesses will usually be subjected to fines from civil penalties, as well as court-ordered damages.

What happens if a company misses payroll?

Missing payroll (and the associated payroll taxes) can result in significant financial penalties under the Fair Labor Standards Act (FLSA). Businesses will often face a variety of penalties and fines if they miss payroll. In addition to paying the unpaid payroll, employers are often required to pay interest or a multiplier to their employees. They will also be subjected to IRS fines. Employees can even take legal action against the business to claim their unpaid wages.

How can I get money to pay my employees?

Proactive steps can ensure you have a legitimate answer to “How to pay my employees,” even when you’re experiencing cash flow issues. Invoice factoring can help you get cash for unpaid client invoices. You could also take out a business loan or line of credit. In an emergency, you could even sell business assets or draw from your own personal finances.

Jim is the General Manager of altLINE by The Southern Bank. altLINE partners with lenders nationwide to provide invoice factoring and accounts receivable financing to their small and medium-sized business customers. altLINE is a direct bank lender and a division of The Southern Bank Company, a community bank originally founded in 1936.