Last Updated May 22, 2026

What do trucking companies, staffing companies, manufacturers, consultants, and all other industries all have in common? They’re all subject to the same common business strain: cash flow problems. And more often than not, cash flow problems and long customer payment terms go hand and hand.

A recent 2025 Quickbooks report revealed that 47% of U.S. small businesses report that at least some of their invoices are overdue by more than 30 days, making slow customer payment one of the most widespread contributors to cash flow instability.

Healthy cash flow is the lifeblood of all businesses. Without adequate reserves of cash, owners stay awake at night thinking about debt coverage, meeting payroll, dwindling inventory levels, covering taxes, etc.

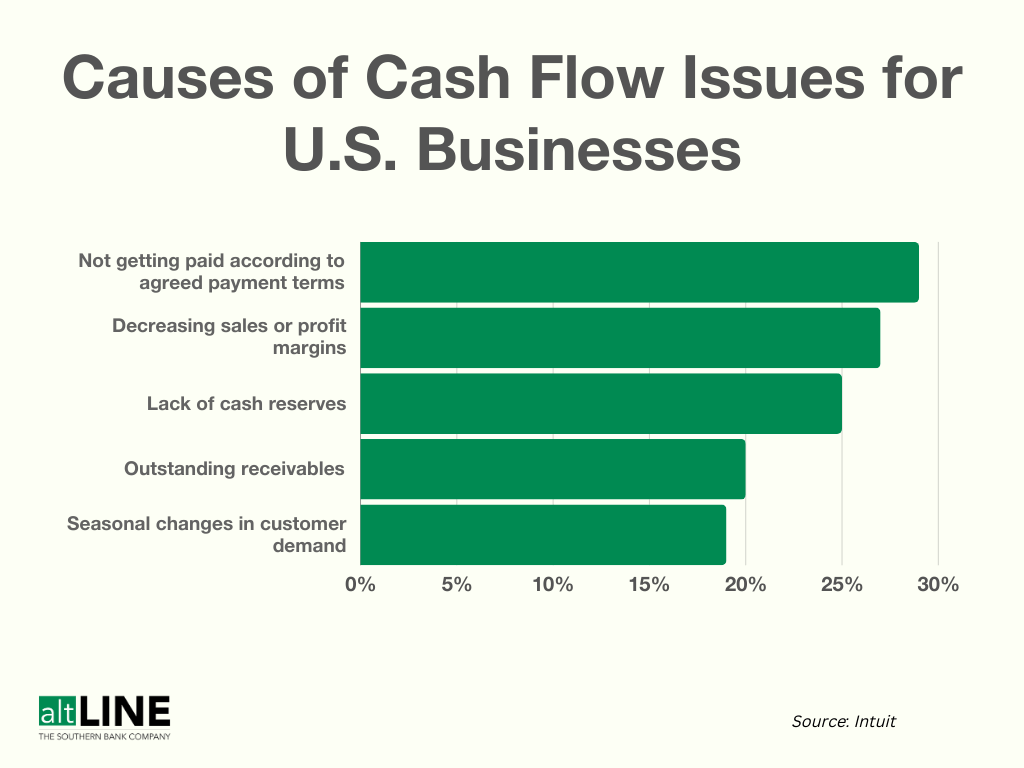

Top Causes of Cash Flow Problems

Cash flow problems is the No. 1 reason small businesses fail.

But this statistic isn’t surprising, nor does it help you overcome your cash flow-related challenges. It’s helpful to know the root causes of cash flow problems so you can move onto solutions for these hurdles that are in your way.

With that said, below are the most common reasons businesses deal with cash flow problems, along with solutions for each obstacle.

1. Late Customer Payment

Delayed customer payments remain a persistent challenge for small businesses, with 2025 data showing that 56% of U.S. small businesses are currently owed money from unpaid invoices, totaling an average of $17,500 per business. As large multi-national businesses continue to stretch their suppliers, the smaller, regional suppliers of raw goods and services are now experiencing the ripple effect. Whether it’s a delinquent customer or a customer with buying power and long-terms, delayed customer payment can cause an enormous strain on your own cash conversion.

Solution: Consider Invoice Factoring

Invoice factoring occurs when businesses sell unpaid invoices to a factoring company in exchange for an immediate advance against the value of each invoice. The business typically receives 80-90% of the invoice value within 24 hours, with the rest being unlocked once the customer submits payment to the factoring company. This is a great way to free up cash flow and particularly common for small and scaling businesses to utilize.

2. Decreasing Sales

Unsurprisingly, one of the biggest triggers for cash flow problems is lower profit margins due to decreased sales.

Fluctuating sales are an inevitably of doing business, but it’s important to brainstorm ways to mitigate this or revert poor sales back to normal if it’s happening with your business. For example, you might need to either increase or decrease your prices or look into offering new products.

Solution: Reevaluate Pricing and Offer Early Payment Discounts

It might sound obvious, but carefully reevaluating your pricing strategy is absolutely necessary if you’re in a sales slump.

One way to intrigue buyers is to offer early payment discounts. For instance, if you’re working on net 30 payment terms, you can include a 2/10 net 30 discount. This means that if they pay within 10 days of the cycle, they get a 2% discount.

Not only could this push them over the edge to partner with your business, but getting paid early will also improve your cash flow.

3. Lack of Cash Reserves, Often Due to Rapid Growth

Sometimes, business owners find their business growing before they have the necessary resources to keep up.

On the surface, rapid growth can hardly be viewed as a bad thing, but unanticipated or swift sales can potentially put a company out of business. More sales means more inventory, more people, and the need for more money.

If your revenue is growing, but your working capital stays the same, that next big customer order you fill could leave you short on cash for your next supplier payment, tax bill, rent check, or loan payment.

Solution: Consider Alternative Financing to Improve Working Capital

One challenge for rapidly growing businesses is qualifying for traditional loans. Often, they still don’t have the collateral, revenue, or operating history to qualify for a bank loan with good rates.

When you’re growing quickly, you need cash quickly. Alternative financing solutions (like factoring) offer a pathway to attaining cash fast. Qualification is easier and quicker than standard bank loans, the approval process is quicker, and funds typically are accessed faster. Aside from invoice factoring, you could explore certain types of lines of credit, peer-to-peer lending, equipment loans, or short-term loans. Just be careful that you’re not taking on too much risk if you have to sacrifice hard assets or a portion of your sales.

4. Outstanding Receivables

When customers are slow to pay or don’t pay on time, it leads to an unhealthy cash conversion cycle. The longer your receivables are outstanding, the longer you’re missing out on potentially valuable working capital that could otherwise be the cash injection you need.

Solution: Sell Your Receivables

Selling your outstanding receivables is the easiest way to solve this common cash flow problem. In addition to invoice factoring, you can try A/R financing, which is very similar to factoring.

5. Seasonality

Perhaps the most common cash crunch amongst customers, excessive seasonality can wreak havoc on a company’s balance sheet. Large cash needs followed by significant cash inflows followed by a quiet season can make planning difficult if not impossible to predict. Having a flexible financing and working capital solution in place can allow business owners to take advantage of seasonal sales rather than succumb to them.

Solution: Create Pro Forma Financial Statements

There are a few types of funding specifically tailored for seasonal businesses. However, an even more proactive solution is to conduct a pro forma analysis.

A complete pro forma analysis involves building cash flow forecasts, a pro forma balance sheet, and a pro forma income statement. This means that you’re predicting future finances. This way, you’ll be fully prepared for seasonal fluctuations and you’ll have a better idea of what to expect.

Benefits of Improving Customer Payment

By collecting cash from customers faster and withholding payment to suppliers longer, companies are able to increase their own cash positions and redeploy that money for their own benefit (increase dividends, initiate stock buybacks, invest in their supply chain, hire new employees, etc.). Essentially, powerful buyers are utilizing their suppliers as a free form of debt.

The strain that slow payment inflicts on the supplier is undeniable. When once-healthy businesses find themselves with cash flow problems and their unable to pay their own suppliers, take on new orders and pay their employees, they then struggle to keep their own doors open. In fact, small businesses most affected by late payments are 1.7x more likely to rely on business credit cards and carry significantly higher balances, increasing financial risk and long-term costs when customer payments are delayed.

When you improve (accelerate) customer payment, you in turn accelerate your cash flow. It allows you to more easily grow or expand your business, pay your employees, and create new and improved products. Plus, putting in the effort to find healthy workarounds for paying invoices with your buyers can by effect enhance your relationship with them if done the right way.

How to Improve Customer Payment

The business owner that finds him or herself on the wrong end of a one-sided buyer/supplier relationship with little hope to negotiate has a few options. Some of which include:

- Fire the problematic customer. This of course assumes dropping the customer will not cripple the business’s growth or long-term viability. This should be a last-resort tactic.

- Grow your own cash reserves. Perhaps the cheapest and most difficult way to solve cash flow problems is to reduce cash outflows. Whether it be cutting costs, delaying payments, or collecting other receivables faster, companies must make difficult decisions in order to conserve cash.

- Ask their supplier if they offer supply chain finance. Many large buyers are offering to finance their supplier’s working capital through prearranged agreements with third-party banks. These rates are typically much lower than what the small business could secure on its own.

- Be transparent with your problematic customer(s). Fellow business owners should understand what you’re going through. Simply being honest and letting them know that their payment habits are inhibiting your cash flow or overall progress can go a long way to mending the relationship.

- Try early payment discounts. Early payment discounts are a common workaround when the supplier needs cash faster than the buyer can provide it. For example, a 2/10 net 30 payment discount means that the buyer receives 2% off of the product or service if they pay within 10 days. This encourages prompt payment.

- Consider invoice factoring. By partnering with a small business lender like altLINE, companies can increase their working capital through a variety of products and services that prevent dangerous cash crunches while continuing to supply their large strategic customers.

Use some of our email templates for collecting overdue invoices if you’re struggling with how to get started.

Using Factoring to Solve Cash Flow Problems

Invoice factoring is a great tool for solving business cash flow problems.

Factoring involves selling your accounts receivable to a third-party factoring company in exchange for cash up front. This type of financing offers faster, easier approval, and is also a scalable solution that can grow with your business. Unlike traditional loans, factoring is not considered debt and thus does not impact your credit.

If your business is faced with cash flow problems or you’re interested in increasing your cash reserves through bank financing, feel free to reach out to talk to one of our representatives at (205) 607-0811 or fill out our free factoring quote form.

Grey was previously the Director of Marketing for altLINE by The Southern Bank. With 10 years’ experience in digital marketing, content creation and small business operations, he helped businesses find the information they needed to make informed decisions about invoice factoring and A/R financing.