Last Updated January 14, 2025

Business owners often look to profit and revenue as key determinants of success. However, a company’s overall financial health also coincides with another equally important measure — cash flow. While most established businesses boast a consistent stream of positive cash flow, it’s not uncommon for startups and small businesses to, at some point, contend with negative cash flow.

Before analyzing negative cash flow, including how to manage or improve cash flow, it’s important to understand what cash flow is and how it can affect a business’ operations.

What Is Cash Flow?

Cash flow is the net amount of money transferred in and out of a company. Though a simple concept to understand, it can often be overlooked in terms of importance. Managing cash flow has proven to be the main component for determining a company’s growth.

Business owners strive for positive cash flow, but it’s more than likely new or small business owners will experience negative cash flow.

What Is Negative Cash Flow?

Negative cash flow simply means a company has more money moving out than money moving in. Cash flow management is an all but inevitable challenge that new business owners face; however, problems arise when it develops into long-term cash flow problems.

Is Negative Cash Flow Bad?

No, negative cash flow is not fundamentally bad. Since running a business is expensive and expenses will almost always outweigh profit early on, dealing with negative cash flow is not always a cause for concern. However, if not properly controlled and addressed, it will cause serious issues for businesses, leading to dwindling working capital.

Example of Negative Cash Flow

| Description | Cost |

| Operations | |

| Cash receipts from customers | $50,000 |

| Cash spent | -$40,000 |

| Investing | |

| Cash receipts from sale of equipment | $5,000 |

| Cost for equipment | -$10,000 |

| Financing | |

| Loan payment | -$10,000 |

| Net Cash | -$5,000 |

This routine cash flow statement reveals that the business has negative cash flow (and also shows the importance of creating and understanding cash flow statements).

What Causes Negative Cash Flow?

Below are some of the most common reasons businesses become cash flow negative.

Expansion

Your business is growing. You’ve decided to move to a bigger warehouse, acquire new office space, hire more employees, or even expand into another city.

These are great benchmarks for a growing company, yet it may steer the company toward negative cash flow until the new location and its employees start generating revenue that matches the expansion expenses. This is why it’s vital to develop business growth strategies in the company’s infant stages to prevent growing too quickly or tumbling into a cash flow deficit.

Inaccurate Product Pricing

Pricing products is one of the most complex yet pivotal tasks a product manager or business owner will face. Performing market research on products your business sells is critical to ensure you are charging the right amount for those products or services. If you’re selling for well over or far less than market value, it will impact your net profit margin and could ultimately lead to negative cash flow.

Low Profits

To avoid low profits, revenue must outweigh outgoing costs; however, new businesses often struggle to cover their initial expenses due to slower sales and startup costs, which leads to negative cash flow.

But once a new business has grown and is well-established in the market, maintaining positive cash flow should be a priority and is a sign of a financially healthy organization.

Causes of low profit can include:

- Unforeseen operating costs

- Unproductive employees

- Mispriced goods or services

- Overhead costs

- Low sales

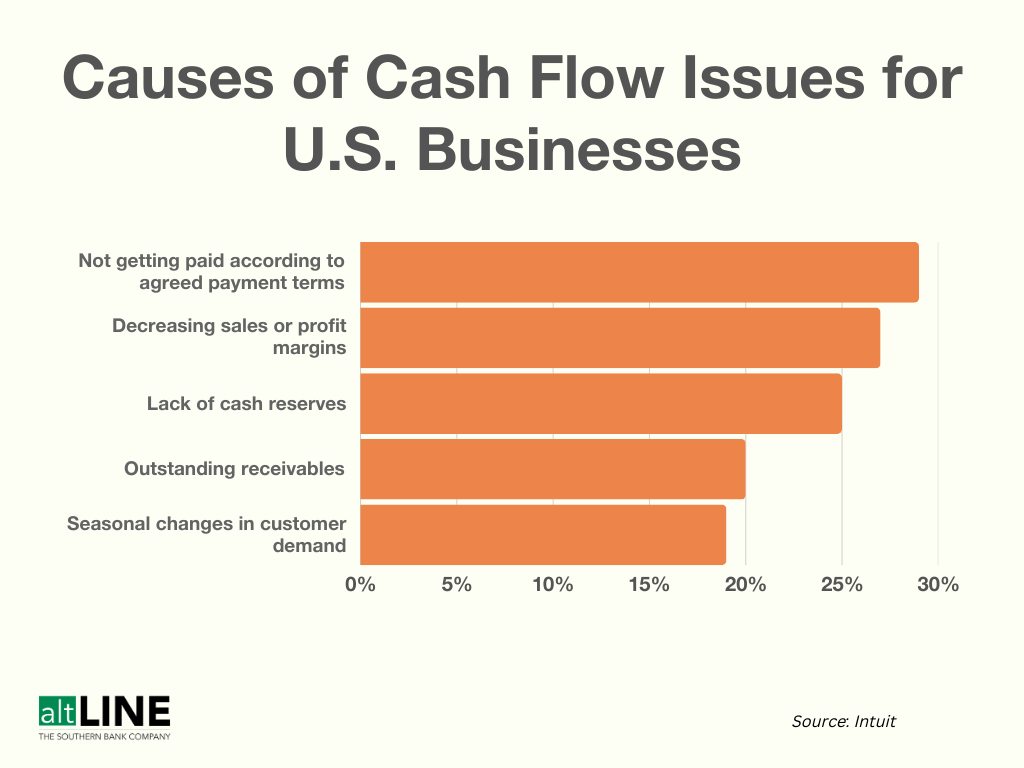

Late Customer Invoice Payments

According to Quickbooks, more than a quarter of small businesses deal with late invoice payments of 30 days or more. More than half said that late payments were the biggest contributor to cash flow problems. Unfortunately, this is an inevitable aspect of business.

However, stunted cash flow due to accounts receivables problems can be minimized thanks to alternative financing methods such as invoice factoring or A/R financing. If you’re struggling with negative cash flow due to late customer payments, researching which financing method makes most sense for your industry could help improve cash flow.

Unaccounted Expenses And Overhead Costs

Any business owner should be prepared to have unexpected financial expenses and other overhead costs when planning a budget or cash flow forecast. It may not be possible to project the exact cost for expenses like equipment maintenance, taxes, and insurance premiums beforehand, but it’s important to make room for and expect these costs when planning so that they don’t alter projected cash flow.

Poor Financial Planning

Among every cause of negative cash flow, failing to plan expenses beforehand is the most avoidable. If you fail to audit your cash flow and accounts receivables, create a cash flow statement, practice cash flow risk management, or calculate your cash flow margin, you are putting your business at higher risk of negative cash flow.

Effects Of Negative Cash Flow

Business owners should prioritize cash flow management just as much as revenue or profit. Running a business with extended periods of negative cash flow is not a recipe for success nor is it sustainable, which can result in disastrous ramifications.

Cost-Cutting

Businesses turn to cutting budgets to reduce expenses once there is evidence of a negative cash flow cycle. Slashing costs not only directly impacts businesses financially but can also create an entirely separate business management problem – employee dissatisfaction. Studies show that when businesses cutback in operating costs, employee experience, engagement, and productivity are all reduced.

Impeded Growth

Negative cash flow prevents businesses from reaching financial goals and forces business owners to devote attention toward managing cash flow rather than implementing growth strategies. Small businesses can be particularly impeded, with already tight budgets becoming even tighter thus making growth goals unconquerable.

Bankruptcy

Spending more than you’re receiving over a sustained period of time is a dangerous game to play. While sometimes necessary to effectively increase cash inflows, doing so for too long without results can lead to bankruptcy. You must take action immediately when you see signs of financial distress, such as long-term negative cash flow, before it’s too late.

How To Manage Negative Cash Flow

Learning what to do when your business has cash flow problems is vital in ensuring you aren’t stuck managing sustained negative cash flow, which can seriously jeopardize your business.

Learn Your Cash Conversion Cycle

The cash conversion cycle (CCC), or cash flow cycle (CFC), is a formula that tracks cash flow and determines how quickly inventory is selling.

Learning how to calculate CCC is pivotal for small business owners and provides the clearest picture into inventory and how fast it can convert.

If you’re trying to manage negative cash flow, learning your cash conversion cycle can allow you to better understand the changes you need to make to your company’s inventory management, marketing efforts, and accounts receivables in order to get back in the green.

Related: How to Calculate Cash Conversion Cycle

Create A Cash Flow Statement

A business cash flow statement is one of three financial statements that are necessary for running a business. It allows you, lenders, investors, and potential buyers to see where cash is coming into your business and where it is leaving your business. A cash flow statement can quickly reveal if your business has positive cash flow or negative cash flow.

Additionally, cash flow statements allow business owners to see where lies the root of negative cash flow and how to adjust finances going forward. For example, if you regularly see cash going into inventory but sales are down, this could signal that you are purchasing too much inventory at a time, causing your negative cash flow. Creating a cash flow statement can help you more effectively analyze your cash flow and pivot your business strategy, if needed.

Keep Receivables In Order

Even if you run a tight ship and have well-organized accounts receivables, uncontrollable factors such as late customer invoice payments can cause a downturn in cash flow.

One way to keep close tabs on issues that affect cash flow, such as customer debt, is by calculating your accounts receivable turnover ratio, which evaluates a company’s revenue collections process.

If a business has an average accounts receivable turnover ratio of 24, that means they are collecting receivables 24 times per year. The greater the ratio, the more a company is collecting funds from customers.

Learning how to calculate your accounts receivable turnover ratio can help you decipher how to stabilize that ratio if necessary and halt further cash flow hindrances.

Research Alternative Financing Methods

Many businesses struggling with negative cash flow are new or small businesses that may not yet qualify for a traditional bank loan.

Alternative financing methods such as invoice factoring can assist these growing businesses with an influx in cash flow. In fact, some of these types of financing do not involve a loan or line of credit but rather offer cash advances aimed to accelerate cash flow. Keep reading to see some of the most popular types of alternative financing.

Four Alternative Financing Methods to Help Manage Negative Cash Flow

The below alternative financing solutions can help you combat cash flow challenges and quickly improve operating working capital.

1. Invoice Factoring

Invoice factoring involves three parties:

- The business

- The debtor (customer)

- The factoring company (factor)

Invoice factoring occurs when a business sells an unpaid customer invoice to a factoring company in exchange for a cash advance (typically 80-90% of the invoice value). The debtor, who is notified of this process through a notice of assignment, then sends the invoice payment to the factor, rather than the business.

Once the factor collects the invoice payment, the remainder of the invoice value (10-20%) is forwarded on to the business, minus a small factoring fee.

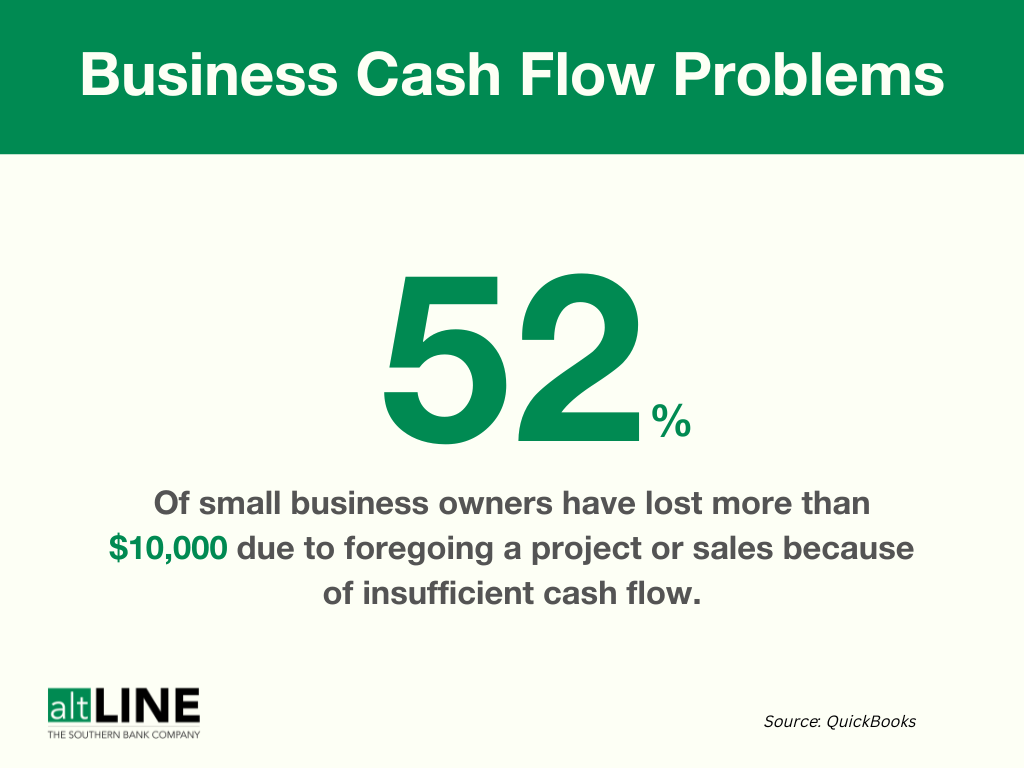

Invoice factoring’s main aim is to improve cash flow and working capital, particularly for small businesses. According to Forbes, cash flow is the biggest obstacle small business owners face, and the average business having over $50,000 in outstanding receivables doesn’t help. This is a major reason why small businesses use invoice factoring as an alternative financing method.

2. A/R Financing

Like invoice factoring, A/R financing (or accounts receivable financing) helps small businesses improve liquidity.

The two alternative financing methods are similar and both involve a third-party factoring company. But with A/R financing, the receivable is collateral for the loan, whereas invoice factoring involves the sale of the receivable to the factoring company.

3. Lines of Credit

A line of credit (LOC) is a set dollar amount a business can use as needed. It’s important to determine whether a secured line of credit or unsecured line of credit makes the most sense for managing negative cash flow, as secured lines of credit require at least some collateral.

Lines of credit can be beneficial to manage negative cash flow; however, a difficult approval process and the danger of relying on LOC’s too much can deter businesses from this financing method.

Related: Invoice Factoring vs. Bank Line of Credit

4. Merchant Cash Advances

A merchant cash advance (MCA) can attract small business owners in need of quick cash. It gives businesses a cash advance based on a percentage of future credit card or debit card sales and is popular for its quick, paperless application process and easy approval criteria.

While it can provide short-term relief, many business owners end up trying to figure out how to get out of a merchant cash advance due to several disadvantages such as unfavorable costs, high risk, and long-term negative cash flow impacts. To get an idea of how much a merchant cash advance may cost you, check out our MCA calculator.

Michael McCareins is the Content Marketing Associate at altLINE, where he is dedicated to creating and managing optimal content for readers. Following a brief career in media relations, Michael has discovered a passion for content marketing through developing unique, informative content to help audiences better understand ideas and topics such as invoice factoring and A/R financing.