Last Updated December 16, 2025

An important measurement of your business’s financial health and liquidity, working capital shows whether you are able to cover all of your expenses in the near future. Because of this, any decrease or increase in working capital is worth paying close attention to. What’s even more important is understanding the root cause of these working capital changes so you know where to make adjustments.

Continue reading to bolster your working capital management skills. Doing so will enhance your decision-making regarding your business’s finances, giving you a leg up over your competitors.

What Is Change in Working Capital?

Change in working capital equals the difference in your net working capital between accounting periods (such as a month or quarter). For example, if your net working capital was $200,000 in June but only $170,000 in July, then you experienced a $30,000 decrease in working capital.

As a business’s assets and liabilities change, you can expect there to be a change in net working capital as well. Every business will experience working capital changes over essentially any given period of time. Depending on your business activities during a particular period, you could see a significant change in working capital or not much change at all.

What Causes Changes in Working Capital?

There are several factors affecting working capital, either positively or negatively. The following are a few examples of actions that can increase or decrease working capital:

1. Accounts Receivable and Accounts Payable

A business’s accounts receivable and payable have an outsized impact on its working capital. Existing liabilities count against a business’s working capital, while receiving invoice payments increases working capital. However, businesses that don’t have efficient invoicing and collection systems in place often struggle to increase cash flow when clients don’t make timely payments. That’s why streamlining accounting practices is so important. A few ways to do this?

- Invest in accounting software

- Eliminate accounting errors by practicing invoice verification

- Consider invoice factoring

2. Inventory Management

When working capital is tied up in excess inventory, it can reduce liquidity. However, when a business optimizes its inventory levels, it can ensure sound working capital management. Selling inventory at a profit will increase working capital and cash flow, but selling at a loss (or having inventory become obsolete and therefore less liquid) can decrease working capital.

3. Business Purchases

When a business uses cash to purchase new equipment, expand a building, or make another similar investment, its working capital decreases. This is because the purchased asset usually isn’t as liquid as the cash. Such purchases must also be noted on the business’s cash flow statements.

Obviously, purchasing equipment is essential. So, it’s not a matter of limiting the equipment or goods you purchase, but rather avoiding making purchases that ultimately aren’t worth the investment. Do your due diligence and verify that your business’s needs truly warrant these new expenses to avoid wasting working capital.

4. Loans

Long-term loans that replace short-term liabilities can actually increase working capital by reducing current liabilities. However, short-term loans that accrue significant interest can decrease working capital.

5. Cash Investments (or Injections)

Net working capital can increase if company ownership or other stakeholders invest additional cash. Doing so increases assets without affecting short-term liabilities, which can greatly increase working capital.

6. Business Expansion

On the other hand, if a company uses its cash to fund a building expansion, working capital will decrease because the company no longer has access to a short-term asset (cash), which was used to fund a long-term asset (which doesn’t count toward working capital).

How to Calculate Change in Working Capital

Calculating the change in working capital is relatively straightforward. For each period (be it a month, quarter, or year), start by totaling your business’s current short-term assets. Then subtract its current liabilities.

(Short-Term Assets) – (Short-Term Liabilities) = Net Working Capital

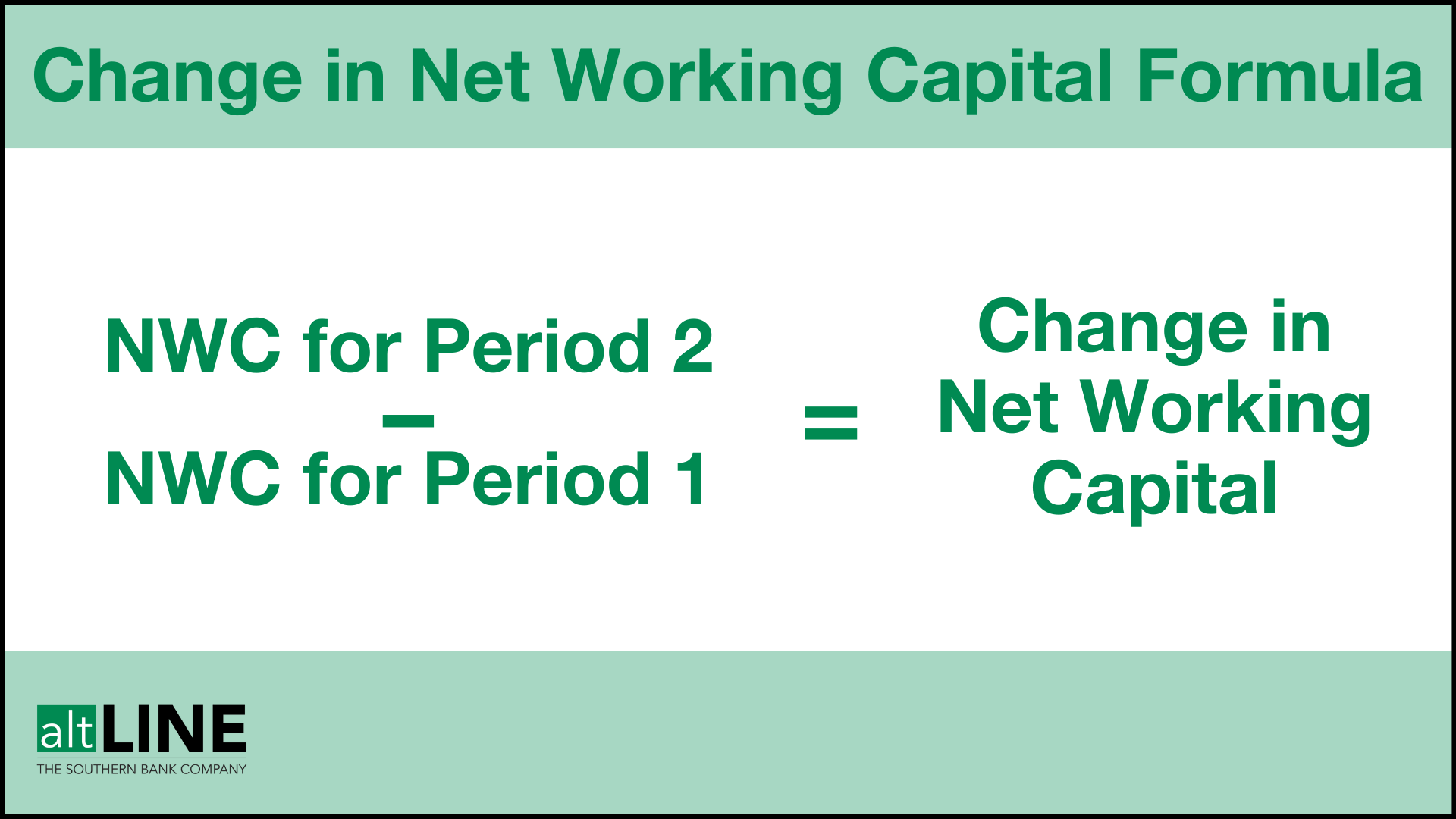

Doing this for each measurement period will make it easy to track changes in working capital moving forward. Once you’ve calculated your net working capital for two (or more) given periods, you can find your change in working capital using the formula below

(Net Working Capital for Period 2) – (Net Working Capital for Period 1) = Change in Working Capital

For example, if you measure your working capital monthly, you could take your net working capital for July and subtract the net working capital for June to track the change. A positive result means working capital has increased, while a negative number means it has decreased.

Change in Net Working Capital Example

Let’s say a company started the month with a net working capital of $100,000. Owners invested an additional $50,000, resulting in a positive change of $50,000 (and a total working capital of $150,000). However, the company then used $120,000 to fund its building expansion, leaving it with just $30,000 in working capital at the start of the next month. The change in net working capital would be recorded as:

$30,000 – $100,000 = -$70,000

Net working capital decreased by $70,000 over the measured time period.

How Can Changes in Working Capital Affect Your Business?

Both positive and negative changes in working capital will affect your business. When working capital increases, your business will have improved liquidity. This means it has a better ability to meet its short-term obligations, such as paying employees or suppliers or making loan repayments. The additional financial stability from a positive change in working capital can also give the company more funding for expansion efforts.

A negative change in working capital will reduce liquidity, making it harder for a business to meet its financial obligations. For example, if a business is unable to meet its loan repayments due to decreased working capital, its lenders could levy additional penalties or raise interest rates. The business could even default on its loan. This financial instability can hurt a business’s creditworthiness and limit funding opportunities.

Tips to Increase Working Capital

Understanding how to improve working capital is essential for ensuring you have enough assets to meet your liabilities. Following a few key practices (particularly in regard to invoicing) will help you increase working capital to improve financial stability.

1. Improve Invoicing Processes

One 2022 study found that 58% of small to midsize businesses experience late payments from customers. Being forced to wait long periods of time for payment can drastically affect working capital and is a leading cause of small business cash flow problems.

A variety of invoicing improvements can improve working capital and cash flow. Sending invoices quickly, sending payment reminders, shortening payment terms, and offering early payment discounts or late fees are a few strategies that business owners use to help reduce late payments. Some businesses also use invoice factoring, in which they sell outstanding invoices to a factoring company for cash.

2. Improve Inventory Management

Carefully tracking how much stock you need to order (and when) helps keep capital from getting tied up in excess inventory. Sound inventory management can also help businesses avoid product shortages that might result in lost sales. Such practices ensure that inventory remains a short-term asset that can easily be liquidated for cash.

3. Renegotiate Payment Terms

Businesses that have good relationships with suppliers and lenders will typically be in a better position to renegotiate their payment terms. Renegotiating to obtain longer payment terms or lower interest rates on loans can improve working capital by reducing your short-term liabilities.

For example, if you’re working on net 30 terms with a business partner, open discussions about potentially shortening the terms to net 15.

4. Try Invoice Factoring

To improve accounts receivable efficiency, many small business owners choose to utilize invoice factoring, a popular alternative financing solution where outstanding invoices are sold to a third-party factoring company in exchange for a cash advance on each invoice.

Changes in Working Capital FAQs

Why did I see a negative change in working capital?

A negative change in working capital occurs when total working capital decreases from one period to another. This is usually the result of a company increasing its total accounts payable or spending cash on long-term (and less liquid) assets. A negative change in working capital could be indicative of a one-time event or it could be the result of an ongoing issue, such as poor management of accounts receivable. Consistent tracking of changes in working capital can be key to understanding the trend of your business’s financial health.

How does working capital affect cash flow?

When changes in working capital involve an increase or decrease in cash, it will be reflected on the cash flow statement. For example, using cash to buy inventory will decrease cash flow because the business no longer has that cash readily available. However, the total working capital will remain the same since the new inventory will be considered a liquid asset. Remember, working capital accounts for all short-term assets, not just cash.

How can changes in working capital help you calculate free cash flow?

Working capital serves as a measurement of a business’s short-term assets (including cash, inventory, and accounts receivable), minus its short-term liabilities (such as payroll, taxes, and accounts payable). Free cash flow (FCF) measures a business’s cash from operations minus its capital expenditures. Notably, FCF accounts for equipment and asset spending, as well as working capital changes.

How do I calculate my working capital needs?

Understanding how much working capital you need is essential for keeping your business operating smoothly while also having enough cash to invest in future growth. A good method to calculate your working capital needs is to use the current ratio, which divides current assets by current liabilities. Generally speaking, a current ratio between 1.5 and 2.0 is considered good, while a ratio of less than 1.0 indicates your business may not have enough liquid assets to cover its current liabilities.

Michael McCareins is the Content Marketing Associate at altLINE, where he is dedicated to creating and managing optimal content for readers. Following a brief career in media relations, Michael has discovered a passion for content marketing through developing unique, informative content to help audiences better understand ideas and topics such as invoice factoring and A/R financing.