Last Updated July 7, 2026

Payment cycles can be notoriously long in the construction industry, and late customer payments often force companies and contractors to wait even longer to get paid. Eventually, these delays create a frustrating cycle of negative cash flow and mounting debt. This is where construction factoring companies come into play.

Construction factoring companies provide cash advances to keep your construction company growing, competitive, and less reliant on customer payment habits to dictate your cash flow.

In this article, we discuss how invoice factoring for construction companies works, its benefits, and how it compares to other lending alternatives. Read on to learn how construction factoring services can improve your cash flow and grow your business!

What Is Invoice Factoring for Construction Companies?

Construction factoring is when your business sells invoices to a third-party company (referred to as the “factoring company” or “factor”) in exchange for a cash advance. Construction companies are often paid with invoices, so there is a possibility of payment delays that lead to negative cash flow. Construction factoring is usually used to access working capital when needed, removing your reliance on customer payment timelines.

How Does Construction Factoring Work?

Factoring construction receivables through a factoring company works by turning unpaid invoices into cash for operating expenses and business growth. Factoring also softens the financial blow of late customer payments, reducing uncertainty and letting you make better long-term plans. Instead of waiting on customers to pay their invoices, you can use factoring services to get cash whenever needed.

Here is how the construction factoring process works

1. Submit Your Unpaid Invoices

Factoring companies accept all kinds of unpaid invoices for factoring. However, they generally favor invoices for creditworthy customers and large or medium-sized companies. Additionally, many typically do not factor invoices for delinquent customers or those with limited credit profiles.

If your invoice turnover time is between 30 and 90 days, your receivables are well-positioned for factoring.

2. Receive an Advance Up to 80-90% of Each Invoice Value

You can generally expect a factoring advance rate of up to 90% of the invoice’s face value, deposited between 24 and 48 hours after submission to the factoring company. The timing of your cash deposit may vary depending on job completion.

3. Factoring Company Collects Payment on Your Outstanding Invoices

The factoring company assists your collections team by providing a secure lockbox for your customers’ money and reporting payment progress through an online customer portal. If issues arise, the factor can communicate with customers to resolve them professionally, helping you keep good business relationships.

4. Remaining Value of the Invoice Paid Out

After payment collection, the factor deducts the factoring fee (typically 1-5% of your invoice) and transfers the remaining invoice balance to your business bank account.

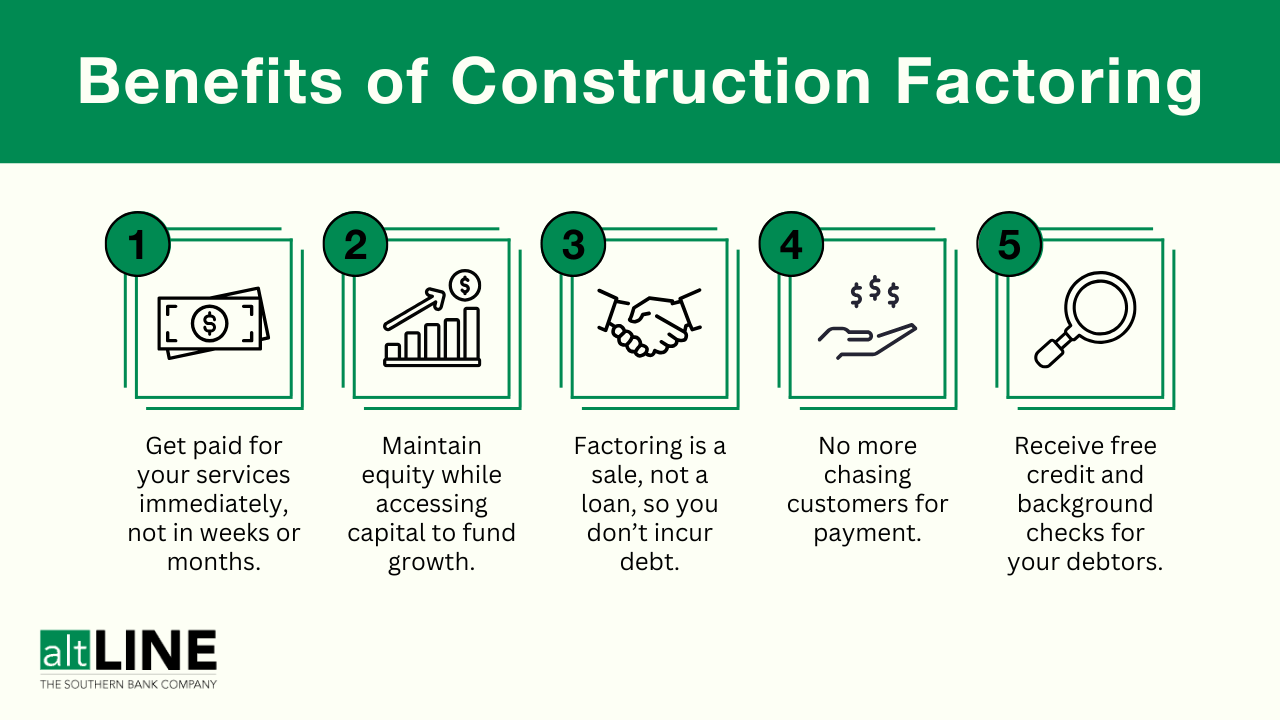

Benefits Of Invoice Factoring For Construction Companies

Construction invoice factoring is a great way to unlock funds when customers are slow to pay by replacing delayed customer payments. Whether you’re an individual contractor or a growing construction company with several employees, here’s how factoring your construction invoices can help:

Get Paid in Days, Not Weeks or Months

The best construction factoring companies fund your invoices within 1 or 2 days. This means you can receive up to 90% of your hard-earned money as soon as possible instead of in 30, 60, or even 90 days.

Access Capital for Business Growth While Maintaining Equity

Business owners sometimes must sacrifice equity to fuel growth, but invoice factoring can set them up for long-term success. Factoring construction invoices gives you the cash needed to fund business growth, pay debts, and meet payroll without sacrificing equity or assets.

Improve Your Cash Flow Quickly

Delayed invoices and late payments can disrupt your cash flow, leaving you unable to grow your business. Construction finance factoring offsets late payments and improves cash flow to ensure your company stays financially healthy.

Back-Office Accounting Help

Construction factoring companies assume collection responsibility for all of your outstanding invoices. This back-end AR management assistance will open up more of your time for driving sales and significantly reduce time spent working on tedious accounting tasks.

Complementary Debtor Background Checks

One underappreciated benefit of construction invoice factoring involves the credit check that companies perform on your debtors. If you’re bringing on a new customer, a factoring company will thoroughly look into their payment history to ensure there’s no evidence of fraudulent activity or late-payment habits.

Uses For Your Factoring Cash Advance

Receiving cash advances from construction invoice factoring means you do not have to wait on customer payments to fund your business. Instead, you can eliminate long payment cycles and unlock growth capital sooner to accelerate business development.

Here are some ways to use cash advances from invoice factoring:

Make Payroll

Paying employees on time is crucial to running a construction business. Unfortunately, late employee payments caused by invoice delays can reduce productivity and delay construction projects.

Invoice factoring cash advances ensure you can make salary payments on time, improving productivity and employee satisfaction.

Take On New Jobs

You should not be forced to wait for customer payments to clear to take new jobs and grow your business. Factoring for construction subcontractors helps you buy the necessary items to complete jobs while keeping your assets and equity intact.

Pay Operating Expenses

Paying for equipment maintenance, material transportation, and building permits with negative cash flow is difficult. Construction invoice factoring gives you a cash advance to pay those obligations without relying on prompt customer payments or sacrificing equity.

Requirements to Qualify for Construction Factoring

Factoring is well-known as one of the most attainable financing solutions for small and new construction businesses. Unlike most forms of business funding, there is no minimum credit score required to qualify. In fact, your credit score is irrelevant to your application.

Instead, a construction factoring company will review and prioritize your customers’ credit history. Remember, it’s their invoices that are being funded. Therefore, the factoring company cares more about their payment habits and credit score than your own.

There are a very few requirements to be eligible for construction factoring cash advances (so few that it’s often considered a no-doc business financing solution). Typically, all you’ll need to provide to qualify is a list of your customers, a completed factoring application, and an AR aging report so factoring companies can examine your customers’ payment history.

Construction Businesses That Can Benefit From Factoring

Factoring companies offer financing services for subcontractors and contractors of all types. Here are some common construction financing services that are offered:

- Building contractor factoring

- Subcontractor factoring

- Construction factoring for bonded jobs

- Factoring for construction material waste disposal

- Commercial constructor factoring

- General contractor factoring

Comparing Construction Factoring vs. Other Alternative Lending Options

In addition to invoice factoring, you have a few other alternatives to improve cash flow. How do these options work, and are they better than invoice factoring? Here is a comparison of the most popular alternative construction financing methods:

Construction Factoring vs. Bank Line Of Credit

Many construction companies choose a bank line of credit as their first financing solution. While construction companies tend to have an easier time qualifying for a bank line of credit, the funds it provides may not be enough to grow their business.

Banks typically approve your line of credit application and set your lending limit by looking at your fixed asset portfolio. Construction companies usually have many fixed assets like machines and vehicles, so they may have an easier time qualifying for a line of credit. But if you are a new construction company that does not have many fixed assets, you may have a harder time getting a line of credit.

Construction factoring is usually the better option for a growing company because the financing company looks at your customers instead of your fixed assets to provide funding. If you work with an established customer base, factoring companies will give you enough working capital when banks cannot.

Construction Factoring vs. ACH/MCA Loans

ACH (automated clearing house) and MCA (merchant cash advance) loans are popular because you can qualify and get funds within one or two days. Thanks to their speed and ease of qualification, ACH and MCA loans are popular among multiple business types.

However, ACH and MCA loans often have high lender and interest fees that can reach 60% of your initial loan amount. If you do not know how to manage large amounts of debt, your company can fall into deep financial trouble.

Construction factoring is considered a less risky alternative to MCAs, because the invoices themselves are the only collateral involved. You also know exactly how much you’ll be paying in factoring fees. With MCAs, rates, fees, and repayments are directly tied to your sales.

Construction Factoring vs Quick Pay Discounts

Offering customers discounted rates for paying their invoices before the due date can improve your cash flow when necessary. However, this method heavily depends on your customers’ priorities.

If your customer prefers having more cash on hand, they may simply ignore your discounted rates and pay their invoice when it’s due, leaving you short on cash and unable to grow your business.

Construction factoring is usually more reliable because you are guaranteed to get a cash advance as long as your invoices are approved.

Typical Construction Invoice Factoring Rates And Fees

Your invoice factoring fees depend on how much you plan to factor and how long customers take to pay. Factoring high amounts and getting customers to pay faster give you the best construction factoring rates. Factoring companies typically also consider other factors like your time in business and customer credit quality.

When factoring an invoice, two types of fees are typically charged:

- Initial fee: This fee pays for your invoice factoring expenses for a set initial period (typically the first 30 days) of your cash advance. It generally costs 0.90-3.50% of your invoice’s total value.

- Incremental fees: These fees cover invoice factoring expenses beyond the initial fee period. They generally cost 0.25-1.50% of your invoice’s total value.

Jim is the General Manager of altLINE by The Southern Bank. altLINE partners with lenders nationwide to provide invoice factoring and accounts receivable financing to their small and medium-sized business customers. altLINE is a direct bank lender and a division of The Southern Bank Company, a community bank originally founded in 1936.