Last Updated July 7, 2026

Waiting 30, 60, or even 90 days for customers to pay can make it difficult to maintain healthy cash flow. Even profitable businesses can find themselves short on working capital when too much money is tied up in unpaid invoices.

One way to solve this problem is by selling your accounts receivable, more commonly known as invoice factoring. Instead of waiting for customers to pay, businesses can sell outstanding invoices to a third party in exchange for an immediate cash advance.

Although this financing option has been around for decades, many business owners still aren’t familiar with how it works or when it makes sense. Below, we’ll explain what selling accounts receivable is, why companies use it, and the advantages and disadvantages to consider before deciding if it’s right for your business.

What Does Selling Accounts Receivable Mean and How Does it Work?

Selling accounts receivable is the process of exchanging unpaid customer invoices for immediate working capital.

Instead of waiting weeks or months for payment, a business receives most of the invoice’s value upfront. Once the customer pays, the remaining balance is released, less an agreed-upon fee.

You’ll often hear this process referred to as invoice factoring, but both terms describe the same financing solution.

Selling receivables is a fairly simple process.

- Your business completes work or delivers products and sends an invoice to the customer.

- You sell that outstanding invoice to a company that purchases receivables.

- You receive an immediate cash advance, often between 80% and 90% of the invoice value.

- Your customer submits payment according to the original invoice terms.

- After payment is received, the remaining balance is sent to your business, minus the agreed-upon fee.

For businesses that regularly invoice other businesses, this creates a more predictable cash flow cycle without having to wait on customer payments.

Why Do Companies Sell Their Accounts Receivable?

Improving cash flow is the primary reason businesses sell their receivables.

Long payment terms or slow paying customers are primary reasons businesses decide to sell outstanding invoices to factoring companies. That’s because these scenarios create financial pressure even when sales are strong. Expenses like payroll, inventory purchases, rent, utilities, insurance premiums, and supplier invoices all have to be paid before many customers settle their invoices.

Companies also choose to sell receivables when they:

- Need working capital to support growth.

- Have customers with long payment terms.

- Want to avoid taking on additional debt.

- Need funding after being denied a traditional loan.

- Experience seasonal fluctuations in cash flow.

Unlike many financing options, selling receivables can grow alongside your business. As invoice volume increases, the amount of available funding generally increases as well.

Who Typically Sells Their Receivables?

Selling receivables is most common among B2B businesses that invoice other companies rather than collecting payment immediately.

Growing businesses, seasonal businesses, and startups often benefit the most because their cash flow tends to constantly fluctuate. Industries with notoriously long payment terms like trucking and manufacturing also see many businesses sell receivables, along with businesses in industries that really need to prioritize making payroll, such as staffing.

B2C businesses that collect payment immediately from customers, such as restaurants, retail stores, and most consumer-facing businesses, generally aren’t good candidates because they don’t generate enough outstanding invoices.

Pros and Cons of Selling Accounts Receivable

Like any financing solution, selling receivables offers both advantages and drawbacks.

| Pros | Cons |

| Improves cash flow quickly | Feed reduce overall profit |

| Flexible source of working capital | Customer credit affects eligibility |

| Few restrictions on how funds are used | You may remain responsible for unpaid invoices |

| Doesn’t create additional debt | Some misconceptions still exist about selling receivables |

| No additional collateral required | |

| Can reduce collections workload |

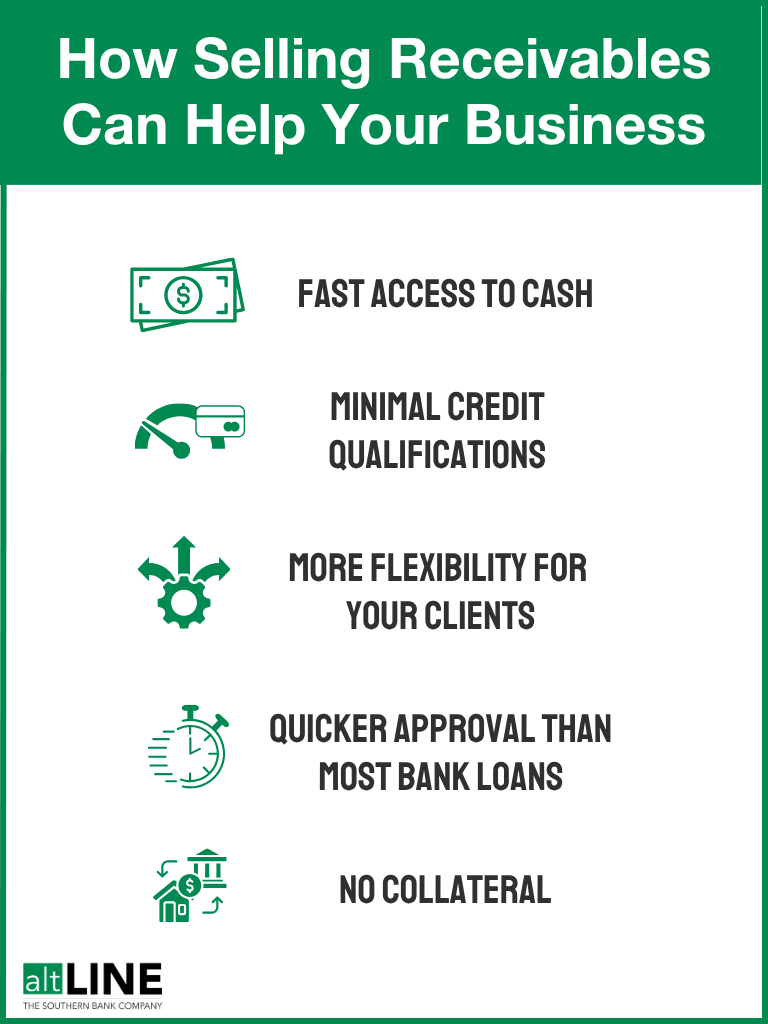

Benefits of Selling Accounts Receivable

Improves Cash Flow Quickly

Instead of waiting weeks or months for customers to pay, businesses receive most of an invoice’s value shortly after selling it. Faster access to working capital makes it easier to cover everyday operating expenses and maintain consistent cash flow.

Flexible Source of Working Capital

As your business generates more invoices, the amount of available funding generally grows as well. That flexibility makes selling receivables especially useful for businesses experiencing growth or seasonal demand.

Few Restrictions on How Funds Are Used

Funds can typically be used for nearly any business expense, including payroll, inventory, supplier payments, rent, marketing, or expansion initiatives.

Doesn’t Create Additional Debt

Selling receivables isn’t the same as borrowing money. Instead of taking on a new loan, businesses convert an existing asset into cash, avoiding future repayment obligations.

No Additional Collateral Required

Unlike many traditional loans, selling receivables doesn’t involve sacrificing equipment, vehicles, or real estate as collateral. The outstanding invoices themselves are the primary asset involved in the transaction.

Can Reduce Collections Work

Many companies that purchase receivables also assist with collections and accounts receivable management. This can reduce administrative work and free up time to focus on other areas of the business.

Potential Drawbacks of Selling Accounts Receivable

While selling receivables can solve cash flow challenges, it isn’t the right solution for every business. Before moving forward, it’s important to understand the potential downsides.

Fees Reduce Overall Profit

Receiving payment early comes at a cost. Fees vary based on factors like invoice volume, customer credit, payment terms, and the size of the relationship, so it’s important to understand the pricing before entering into an agreement.

Customer Credit Matters

Approval depends heavily on the creditworthiness of your customers. If your customers have a history of late payments or poor credit, some invoices may not qualify.

You May Still Be Responsible for Non-Payment

Many receivables purchase agreements are structured as recourse arrangements, meaning the business may remain responsible if a customer ultimately doesn’t pay an invoice. Review the agreement carefully so you understand when that responsibility applies.

Misconceptions Still Exist

Some business owners still associate selling receivables with companies in financial trouble. In reality, businesses of all sizes use it to improve cash flow, support growth, or manage long payment cycles.

Selling Accounts Receivable vs. Taking Out a Business Loan

Although both selling receivables and taking out a loan provide a working capital boost, they function very differently.

A traditional business loan gives you a lump sum that must be repaid over time with interest. Approval is largely based on your business’s financial history, profitability, and credit profile.

Selling receivables works differently. Instead of borrowing money, you’re converting unpaid invoices into immediate cash. Since funding is tied to your outstanding invoices, businesses with limited operating history or less-than-perfect credit may still qualify if they invoice reliable customers.

Neither option is inherently better than the other. The right choice depends on your company’s financial situation, funding needs, and long-term goals.

However, for many business owners, traditional loans are unattainable due to stringent qualification requirements, such as minimum credit scores or significant collateral. That’s why invoice factoring has become such a popular alternative financing solution for startups and growing businesses.

Is Selling Accounts Receivable Right for Your Business?

Selling receivables can make sense for businesses that routinely wait weeks or months to receive payment from customers.

You may benefit if your business:

- Primarily sells to other businesses

- Offers payment terms of 30 days or longer

- Has customers with strong payment histories

- Needs more consistent working capital

- Wants to improve cash flow without taking on additional debt

How altLINE Can Help

altLINE has more than 90 years of experience purchasing B2B receivables and helping business owners achieve their growth goals by stabilizing cash flow. Since we are a bank factoring company, we are FDIC-insured and state and federally regulated, ensuring full transparency and security.

If you’d like to learn more about selling receivables or want to determine whether it makes sense for your business, we would be happy to answer your questions. Fill out our invoice factoring quote form and we will be in touch or reach out to us at +1 (205) 067-0811 to speak with one of our representatives immediately.

In Summary: Selling Accounts Receivable

Selling accounts receivable gives businesses a way to access working capital without waiting for customers to pay outstanding invoices. For companies dealing with long payment terms, it can create more predictable cash flow while providing additional flexibility to cover operating expenses and pursue growth opportunities.

Like any financing solution, selling receivables has both advantages and disadvantages. Understanding how the process works, what it costs, and when it’s most appropriate can help you determine whether it aligns with your business’s financial needs.

Selling Accounts Receivable FAQs

Can you legally sell accounts receivable?

Yes. Businesses commonly sell outstanding invoices to companies that purchase receivables in exchange for an immediate cash advance. Once the transaction is complete, the purchaser collects payment directly from the customer according to the original invoice terms.

Is selling accounts receivable the same as invoice factoring?

Yes. Invoice factoring is simply the formal name for selling accounts receivable. Both terms describe the same financing process.

Is selling receivables considered a loan?

No. Selling receivables isn’t a loan because you’re converting an existing business asset into cash rather than borrowing money that must be repaid over time.

What’s the difference between selling receivables and invoice financing?

When selling receivables, ownership of the invoices is transferred in exchange for immediate cash. With invoice financing, the business keeps ownership of its invoices while borrowing against their value and continuing to collect payment from customers.

How quickly can businesses receive funds?

Funding timelines vary by provider, but once an account has been established, businesses can often receive an advance within one or two business days after approved invoices are submitted.

Grey was previously the Director of Marketing for altLINE by The Southern Bank. With 10 years’ experience in digital marketing, content creation and small business operations, he helped businesses find the information they needed to make informed decisions about invoice factoring and A/R financing.