Last Updated May 13, 2026

For many businesses, qualifying for traditional financing can prove difficult, and it doesn’t help that banks have become increasingly strict when reviewing business loan applications in the post-COVID era.

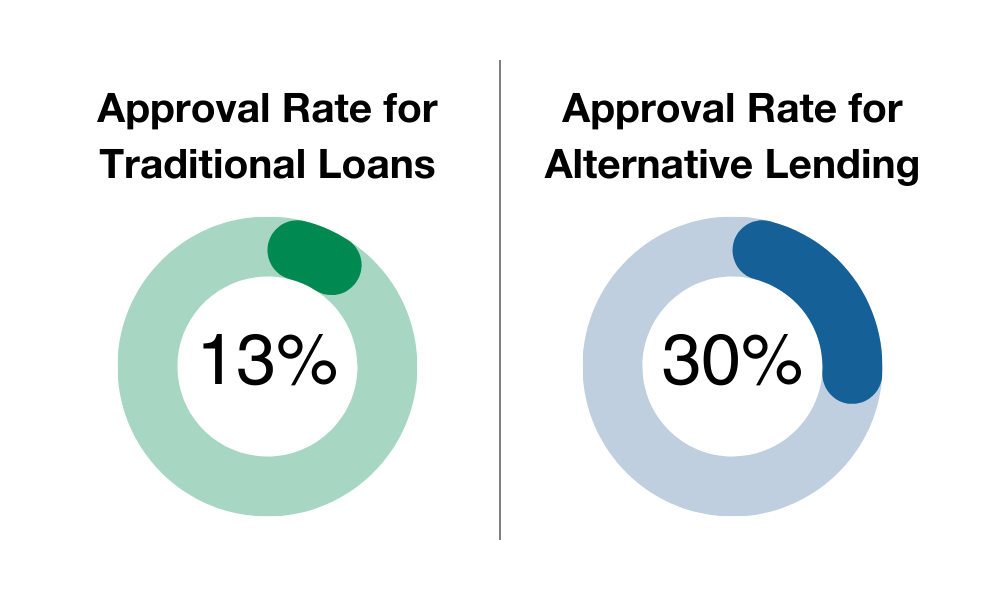

Thankfully, there’s a different form of financing that is much easier for certain types of businesses to qualify for – alternative lending. While just 13% applications for traditional loans were approved in November 2023, 30% of applications for alternative lending solutions were approved in the same month.

If you run a business, it’s essential to explore alternative lending because, in some cases, alternative lending can lead to even more fruitful financial outcomes than traditional lending.

This comprehensive alternative business financing guide will walk you through the key things you need to know before seeking out funding.

What Is Alternative Lending?

Alternative lending is any form of financing that involves non-traditional banks or credit unions. It is designed for businesses that have a tough time qualifying for traditional financing solutions, especially those that need funds fast. Therefore, most forms of alternative lending are easier to qualify for than traditional bank loans.

Characteristics of Alternative Lending Solutions

If you’re wondering if a certain form of financing falls under the “alternative lending” umbrella, consider the following characteristics that generally define alternative lending solutions:

- No minimal credit score required to apply

- Easier and quicker approval

- Elevated interest rates

- Shorter repayment terms than a traditional loan

- Fast funding times

- Minimal documentation and paperwork required when applying

Which Types of Businesses Benefit from Alternative Lending?

Alternative sources of financing for businesses have a reputation for being particularly flexible for the following types of businesses:

New Businesses

Because 20% of businesses don’t survive more than one year, big banks often won’t accept traditional financing applications from brand new businesses in order to protect their funds.

New businesses can seek refuge by turning to alternative lenders. Alternative solutions generally offer increased flexibility, so new businesses won’t have to worry about what might happen if, for whatever reason, funding needs suddenly increase or diminish. Lenders are understanding in these situations and are aware that startups’ plans, processes, and needs are constantly changing.

Small Businesses

Small businesses are usually operating on a tighter budget than larger companies with more immediate funding needs. For example, just one instance of a customer being unable to pay for the provided goods or services can quickly derail a small business’s cash flow, jeopardizing plans.

Thankfully, approval for alternative lending is faster than when applying for a standard bank loan, and funds can be released quicker. This means small business owners can spend less time sweating their approval statuses and waiting for those funds to hit their accounts.

High-Growth Businesses

These business loan alternatives are a great fit for businesses that are expanding operations or are in high-growth periods. With many alternative lending solutions, credit lines can be adjusted over time as growth occurs and funding needs are elevated.

Further, some options don’t require businesses to provide collateral, which can be a relief for growing startups as they don’t have to risk vital assets that can’t be lost.

Related: Funding for High-Growth Businesses

Seasonal Businesses

Traditional lenders might be wary of approving seasonal businesses due to their significant annual fluctuations in cash flow, revenue, and profit.

Because certain alternative financing options offer adjustable lines of credit, lenders and borrowers are able to easily communicate changes in funding needs as the seasons change.

Alternative Lending Examples

Before deciding on a form of financing, it’s good to have a grasp on all of the lending options at your disposal. Additionally, not every alternative lender is as reliable as the next, so it’s recommended to speak with multiple lenders, perhaps utilizing your network to ask for recommendations as well.

With that being said, below are some of the most common types of alternative lending.

Invoice Factoring

Invoice factoring is the process of selling your receivables (or outstanding invoices) to a third party in exchange for cash upfront. This is a preferred option for B2B companies that suffer from long payment terms or slow-paying customers and need to immediately improve working capital or cash flow.

Qualification is dependent on your customers’ creditworthiness, not your own, making it a great alternative financing solution for small businesses and new businesses that might not have the business credit necessary to qualify for other loans. Once you apply, a factoring company will evaluate your business’s customers, reviewing their past payment histories and likelihood of paying their invoices. To properly evaluate your customers, factoring companies will perform credit checks and examine your accounts receivable aging schedule.

If approved, a factoring company will purchase your invoices, then immediately advance 80-90% of the cash value to your business (typically within 24 hours). Once the factoring company collects invoice payment from your debtor(s), it will forward your business the remaining 10-20% of the invoice value (minus a small factoring fee).

Factoring is a sale, not a loan. Therefore, it’s a favorable option for businesses looking to avoid further debt or credit balances.

Accounts Receivable Financing

A sister of invoice factoring, accounts receivable financing operates in much the same way. However, accounts receivable financing is a loan, not a sale of your invoices. Therefore, an A/R financing company will use your outstanding invoices as collateral against a loan. Unlike invoice factoring, where the factoring company owns your invoices, you retain ownership and collection of your receivables.

Asset-Based Lending

By definition, asset-based loans fall somewhere in between traditional and alternative financing. It is a loan (not a sale) based on the value of designated assets, like machinery, heavy equipment, or real estate. 2

Unlike most forms of alternative lending, collateral is required for asset-based lending (ABL); in fact, these loans revolve around collateral. The bank or other financing provider will hold the assets as collateral for the loan.

Given the higher credit requirements for ABL, new businesses likely won’t be able to secure this type of loan. Instead, asset-based lending is a better fit for larger businesses with hard assets to borrow against and sufficient credit. This makes it an exception from the rest of the loans listed, as an asset-based loan probably won’t appeal to most types of businesses that alternative lending generally appeals to.

That said, many businesses may graduate from a different type of alternative financing to asset-based lending.

MCA Loans

An MCA loan, or a Merchant Cash Advance, is a cash advance based on anticipated future credit and debit card sales. It is typically delivered in a lump sum. The provider will look at daily credit card receipts to determine that the loaned amount can be paid back in a designated amount of time.

MCA loans can be very expensive in terms of APR, with rates anywhere from 10%-150% depending on payback terms and the amount borrowed. Some providers can be predatory with extremely high interest rates, taking advantage of businesses desperately in need of fast cash. Borrowers should beware and be careful if choosing an MCA lender, as they’re sometimes stuck trying to figure out how to get out of an MCA.

The loan is typically paid back in the form of a percentage of credit and debit card sales called a holdback, and payments are made on a weekly or daily basis. For example, the provider may withhold 20% of your daily or weekly sales to be paid back against the loan. Because MCA loans are so expensive, it’s important to weigh the value of the immediate cash flow provided by the loan against the amount of interest paid.

ACH Loans

Much like merchant cash advances, Automated Clearing House loans (ACH loans) are lump sum cash advances. However, unlike an MCA loan, which is determined by daily credit and debit card sales, an ACH loan is based on the average daily balance of your business checking account. ACH loans are then paid back in the form of an automated withdrawal from your business checking account at agreed upon intervals (typically daily or weekly). This type of financing also comes with high APRs, so businesses should be selective about choosing a provider.

Crowdfunding

Crowdfunding involves one or more people coming together to raise money to finance projects, expansion, or purchases. This can be done by asking your network or family and friends, though it’s most commonly achieved through utilizing platforms on the internet such as GoFundMe and Kickstarter.

Peer-to-Peer Lending

Peer-to-peer lending occurs when parties borrow funds from individuals unassociated with financial institutions. This is accomplished thanks to websites solely dedicated to facilitating P2P lending by promoting borrowers and lenders looking for funding and willing to provide funding, respectively.

With peer-to-peer lending, the individuals investing don’t become shareholders but rather receive interest on the loan.

Grants

Government and foundation grants are an age-old source of alternative lending for business owners who need additional funds to properly move forward with a project, research, or other initiative they have in mind. This requires making a pitch to whomever the source is that’s offering the grant.

Grants are a fantastic way to receive funding without having to pay anything back to the supplier, but large grants, in particular, can get very competitive. Government grants can be found on grants.gov, while GrantWatch.gov has a plethora of information on foundation and corporation grants.

Signs Your Business Could Be a Good Fit for Alternative Lending

Maybe your business fits the types of companies that benefit most from alternative financing, but you’re still not sure if it’s the right fit. Here are key signs your business could be ideal for alternative credit.

You Need to Close the Customer Payment Gap

The customer payment gap is the time between invoicing a client and actually receiving payment, which can range from 30 to 90 days. Service-based businesses like staffing agencies, consultants, and manufacturers often struggle to cover payroll and expenses during this gap. Factoring directly solves this problem by providing funds immediately after invoicing, so your business keeps running smoothly without waiting for clients to pay.

Your Business Has Limited Operating History

Startups and young businesses often get denied traditional loans because banks see them as high-risk. Alternative financing offers a faster path to working capital, helping new businesses stay operational and grow even without a long track record.

You Have Poor Credit

Banks rely heavily on your credit score, but alternative lenders focus more on your customers’ creditworthiness. This makes approval faster and easier, especially for businesses that may be struggling with fair or poor credit.

You Don’t Want to Take on Debt

Some alternative financing options, like factoring and crowdfunding, aren’t loans. Factoring allows you to sell invoices for upfront cash while crowdfunding can provide donations with no repayment required. These options keep your credit intact and don’t create liens, letting you preserve funds while growing your business.

Your Business Has Few or No Assets to Borrow Against

Small service businesses often lack the collateral banks require. Factoring and accounts receivable financing bypass this issue by using invoices as the basis for funding. Once approved, these invoices turn into immediate cash, giving your business the working capital it needs without risking hard assets.

How to Choose an Alternative Lending Solution

Once you’ve compared different alternative credit options and targeted which structure fits your financial needs the most, your next step is identifying your alternative funding source.

Below are some tips when going about your search for alternative financing companies.

1. Identify Reliable Lenders With a Good Reputation

The stigma against alternative lending is that it can frequently attract predatory lenders.

While these lenders do exist, they can be eliminated from your search process by doing your due diligence. The best way to do that is by identifying lenders with strong reputations by looking into their customer reviews (via Google, TrustPilot, etc.) and utilizing your network for referrals and advice.

Another way to gauge the reliability of lenders is by getting a representative on the phone and asking questions pertaining to qualification, the potential onboarding process, rates, fees, terms, and other conditions. Listen for clear, sensible answers. If you’re left feeling uneasy, that might be a sign to search for another lender.

2. Prioritize Lenders Backed by a Bank

Factoring is a prime example of alternative credit that can be supplied by either banks or independent companies.

It’s crucial to do your best to partner with a bank. When that term, “predatory lending,” gets thrown around, it’s often in reference to those independent lenders who are far less regulated than banks.

Partnering with an FDIC-insured, state and federally-regulated bank prevents businesses from being taken advantage of by independent providers who don’t have to abide by strict compliance policies. Due to regulations, banks can usually be counted on to have well-organized, clear-cut processes with good customer service as well. Additionally, banks are more likely to be transparent about rates, while some independent lenders will hide fees in the fine print.

3. Read the Terms and Conditions in Contracts

It goes without saying, but ensure all terms and conditions of the partnership are clearly laid out in the contract. Hidden fees are unfortunately common, not just in business financing contracts, but in all types of contracts. In fact, 85% of Americans have been faced with unexpected hidden fees.

An example of something to look out for and note in a factoring contract, for example, is the window of notification. This is the time period where you can back out of a factoring agreement prior to its renewal without being charged fees or additional trouble.

4. Analyze Rates and Fees, But Don’t Let That Be the Only Factor in Your Decision

While non-traditional lenders tend to have higher rates than banks offering standard business loans, sometimes those higher rates might be worth it for your business. Or possibly, imagine a scenario where Lender A might have slightly higher rates than Lender B, but Lender A is backed by a bank, thus more regulated and has a superior reputation and reliable customer service. You might be better suited to work with Lender A.

5. Plan Ahead

Because interest rates tend to be higher with alternative lending options, borrowers must look ahead by projecting future finances to ensure they can afford to obtain alternative credit not just in the present but also down the line. An MCA, for instance, can include very high rates with rigid repayment structures that are difficult, if not impossible, to get out of. In these situations, borrowers might realize that the constant repayment withdrawals and high APR might actually do more harm than good.

You can plan ahead by periodically completing a pro forma analysis, forecasting your three major financial statements: balance sheet, profit & loss statement, and cash flow statement. Forecasting other standard financials, such as sales revenue and profit, should also be completed routinely.

Alternative Lending Pros and Cons

Non-traditional loans and funding options will differ by type. However, there are some general pros and cons to utilizing alternative lending to fund your business. Let’s recap some of the benefits and drawbacks of alternative financing.

| Alternative Lending Pros | Alternative Lending Cons |

| Quick, Easy Approval Processes | Rates Tend to Be Higher |

| Fast Funding | Loan Terms Tend to Be Shorter |

| Unsecured Funds (No Collateral Required) | Lenders Can Be Predatory, Especially If Independent and Not Bank-Backed |

| Can Qualify With Low Credit | Some Options Won’t Build Business Credit |

| Increases Chances of Qualifying for a Standard Business Loan in the Future |

Pro: Quick Approval Process

Qualifying for MCA loans, ACH loans, invoice factoring, and AR financing is much easier and quicker than your typical business loan through a large bank. Requirements are generally less stringent, and for factoring and AR financing, businesses with poor or nonexistent business credit and no hard assets can even qualify without issue.

Pro: Fast Funding

Qualifying isn’t the only accelerated process in the alternative financing industry. Once approved, funds are typically released quicker as well, usually within 24 to 36 hours. Companies that need to improve cash flow fast to stay afloat are thrown a life vest.

Pro: Unsecured Funds (No Collateral Required)

The fact that alternative lending rarely requires hard assets to be eligible is a huge bonus for not just new businesses and startups, but also businesses in certain industries such as staffing and recruiting that simply don’t require many hard assets to successfully operate.

Pro: Can Qualify With Poor Credit

Businesses with poor or nonexistent business credit can qualify without issue for many non-traditional sources of funding, particularly invoice factoring and AR financing. This is because these are accounts receivable-based financing options, meaning the creditworthiness of a borrower’s customers takes priority for the provider.

Pro: Increases Chances of Qualifying for a Traditional Loan in the Future

When reviewing loan applications, traditional banks that offer standard business loans like seeing businesses that have had a successful partnership with a lender in the past, especially a lender that’s backed by a bank. Therefore, alternative lending can be used as a stepping stone for businesses that are eventually trying to secure business loans.

Con: Interest Rates Tend to Be Higher

It’s no secret that interest rates tend to be higher with alternative financing; it’s the drawback of having faster and easier access to working capital.

Con: Term Lengths Tend to Be Shorter

Another drawback of having quicker, easier access to funds is that term lengths are frequently shorter than standard loans. The reason being, lenders don’t want to take on too much risk in releasing funds to new businesses, startups, and other businesses without significant assets or high credit. For instance, MCA loan terms can be as short as three months.

Con: Non-Bank-Backed Lenders (Independent Companies) Can Be Predatory

Alternative lending is defined as any financing solution provided by a non-traditional bank, meaning that it opens the doors for independent, non-regulated lenders to take advantage of desperate borrowers through sky-high interest rates, extremely short terms, hidden fees, and unclear policies. Thankfully, there are many financial institutions that include alternative financing solutions as options, so these predatory lenders can be avoided.

Con: Some Options Don’t Build Business Credit

MCA and ACH lenders don’t report payments to the three major credit bureaus. If your ultimate goal of alternative lending is to build business credit, you should pick one that can improve your track record, such as asset-based lending.

In-Summary: Choosing an Alternative Financing Option for Your Business

What’s most important is that you have a clear picture of your finances so that you end up choosing the best alternative lending option for your business.

It’s important to understand that the best choice for your business might be different from the next business. Consider the following when choosing which financing option best suits your needs:

- Collateral: Some sources of funding will be unattainable without providing collateral for security. Thankfully, many alternative lenders offer unsecured financing.

- Credit: If you have a less than ideal business credit score, you still have financing options. Factoring and ACH loans are viable funding sources for those with poor credit.

- Short-Term Needs: It’s imperative to have as precise an idea as possible regarding how much money you need to keep operations functioning. If you overestimate short-term needs, you’ll end up paying more in rates and fees than you have to.

- Cash Flow (Current and Future): In all likelihood, your cash flow will dictate your funding needs. You should make a habit of periodically creating a cash flow statement and cash flow model to gain insights into your performance and the direction you’re headed.

- Risk: It’s not uncommon for unprepared business owners to get taken advantage of by solely thinking of short-term gains and disregarding long-term effects. Always evaluate risk before obtaining financing, even if you feel like you’re in a very challenging financial situation.

- Fees and Rates: Interest rates differ not only by the financing type but also by the source of the funds. For instance, every invoice factoring company won’t have the same rate and fee structures. Consult with representatives from each company so you can eventually weigh your options.

Finally, keep in mind that having a business loan application rejected isn’t the end of the world. There are numerous alternative credit options out there, each with its own pros and cons. By doing your homework and learning about the options at your disposal, you can bounce back in no time.

Need Alternative Financing? Consider Factoring With altLINE

altLINE has 90+ years of experience helping small business owners reach their growth and expansion goals by factoring their invoices.

Whereas many factoring companies operate independently, altLINE is bank-backed by The Southern Bank Company, meaning we are an FDIC-insured, state and federally regulated bank. We have been acknowledged by sources such as Forbes and Investopedia as a top factoring company nationwide and have earned an A+ rating by the Better Business Bureau and 4.8 rating on TrustPilot.

We take pride in our customer service, so if you have any questions about the factoring process or whether you might be the right fit, feel free to contact us today. We’d be happy to guide you in your decision-making process. You can call one of our representatives at +1 (205) 607-0811 or request a free quote.

Grey was previously the Director of Marketing for altLINE by The Southern Bank. With 10 years’ experience in digital marketing, content creation and small business operations, he helped businesses find the information they needed to make informed decisions about invoice factoring and A/R financing.