Last Updated March 24, 2026

Just about every business will run into issues with available funds at some point. While intermittent cash flow problems are normal, particularly for growing businesses, it’s important to stay one step ahead by securing financing.

But what if you run a small business and can’t qualify for a traditional bank loan or line of credit? Luckily, there are two alternatives: purchase order financing and invoice factoring.

These alternatives are sought after by small business owners because they don’t require high business credit scores to qualify. But it’s important to understand the differences between the two.

Purchase order financing vs. invoice factoring can easily be confused with one another and usually have similar borrower profiles, so let’s break down each of these lending options designed explicitly for small business.

What Is Purchase Order Financing?

A company has the option to secure a loan with purchase order financing (PO financing). This practice allows the company to buy the materials necessary to start the job a client has ordered. This kind of financing is common among importers/exporters, distributors, manufacturers, wholesalers, and contractors.

For instance, a manufacturer receives a large order from a new customer. The order is bigger than any the company has received before and will require more funding than the manufacturer has on hand. It would be difficult to secure a traditional bank loan since the manufacturer cannot demonstrate experience with an order of this size.

Purchase order financing would be ideal for this company. The lender accepts the verified purchase order and directly pays the supplier, who then delivers the product to the customer. The manufacturer then invoices the customer, who pays the lender. The lender then sends the payment to the manufacturer, minus lending fees.

Pros of Purchase Order Financing

Like every alternative lending option, PO financing comes with advantages and disadvantages.

Let’s take a look at what your business can gain by using purchase order financing.

- Easy/Quick Access to Cash: Small businesses often find purchase order financing easier to secure than traditional bank loans. The funds are also usually available much more quickly, sometimes in as little as 24 hours.

- Lender Assumes Collection Risk: The lender usually takes on collection responsibility. The lender, not the small business, risks loss if customers do not make payment.

- Comparatively Low Interest: Using credit cards to pay for upfront materials involves hefty interest rates. Even traditional bank loans can include a substantial price tag in the form of interest. Purchase order financing bypasses this expense.

- Line Can Grow With Revenue: As a small business expands and increases its revenue, a purchase order financial arrangement can grow with it.

- Available to Small Businesses: Unlike traditional loans, purchase order financing is much easier for a small business to secure. Even some startups are eligible for this form of funding.

- Credit Line Determination: A major advantage of purchase order financing is that lenders base their decisions on the creditworthiness of a business’s clients rather than that of the company itself. This practice makes it an especially promising line of credit for new businesses.

Cons of Purchase Order Financing

Here are some potential downsides to consider before moving forward with PO financing:

- Upfront Fee: Most purchase order lenders require an upfront payment. This fee will be due before the customer has paid for services or products.

- A Short-Term Solution: PO financing is a short-term solution to what could be a prolonged problem if you can’t sort out existing cash flow concerns. Plus, PO financing won’t benefit your credit score, so even if you have a long-term arrangement with a lender, succeeding in that arrangement won’t directly benefit your chances of securing more traditional lines in the future.

- Reduced Payments: A small business in a PO financing arrangement will not receive the full payments from customers. Lending fees will reduce these payments.

- Customer Contact: Billing will not directly occur between the business and its customers. The lender will step in as a third party for collection.

- Only Covers Direct Supplier Expenses: Unlike a traditional loan, purchase order financing can only be applied to supply costs. Other expenses will require a different solution.

- Requires Large Margins: Purchase order financing often requires a transaction with gross margins of 25% or higher.

What Is Invoice Factoring?

Another option for small businesses in need of operational funds is invoice factoring. For this type of financing, a company trades its unpaid invoices for a loan of a comparable amount from a factoring company. The business can use the loan to continue day-to-day operations without waiting for clients to pay their bills.

This form of funding is especially common among trucking companies (where it’s called “freight factoring“), staffing agencies, janitorial services, IT consultants, landscaping companies, and other businesses that provide invoicing services after those services have been provided.

For instance, a landscaping company could use unpaid invoices to secure financing to meet payroll, purchase gasoline, and repair equipment. The factoring company, or factor, then collects the payment from the landscaper’s clients.

The primary component that lenders consider in invoice factoring is not the creditworthiness of the borrower but that of the borrower’s customers, the entities who owe the invoice payments. Therefore, this form of lending is generally used for B2B invoices only.

Pros of Invoice Factoring

Small business owners find many advantages of factoring, including:

- Immediate Cash Flow: Invoice factoring provides instant funds (within 24 hours).

- Ongoing Cash Flow: Invoice factoring also provides an ongoing source of fund infusion. As long as a small business is issuing verifiable invoices, this source of funds is viable.

- Better Chance of Approval: Invoice factoring is designed to give small businesses an increased likelihood of approval. Like PO financing, this form of funding examines the credit of a business’s customers, not that of the company itself.

- Outsourcing Billing Tasks: Factoring relieves a small business of much of the billing process. The lender assumes responsibilities for invoice collection.

- No Collateral Required: Small businesses in need of funds do not need to provide collateral.

Cons:

Like every financing option, there are a few drawbacks. Here are some to consider before moving forward with a factoring provider:

- Factoring Fees: Factoring fees can fall anywhere between 1-5%. However, many small business owners who choose to factor their invoices quickly realize that these fees are worth the cash flow boost.

- Responsibility for Unpaid Invoices: While invoice factoring reduces the risk of bad debt, it does not eliminate it. Invoice factors are not collection agencies. If customers refuse to pay their invoices, the liability for those funds falls back on the small business.

- Factoring With Independent Companies Can Be Risky: Invoice factoring is generally a fantastic financing option for small business owners looking to ease their AR responsibilities and find a solution for slow-paying customers. However, if you choose to factor with an independent company instead of a bank, it can present some risk, as these companies aren’t regulated the same way banks are.

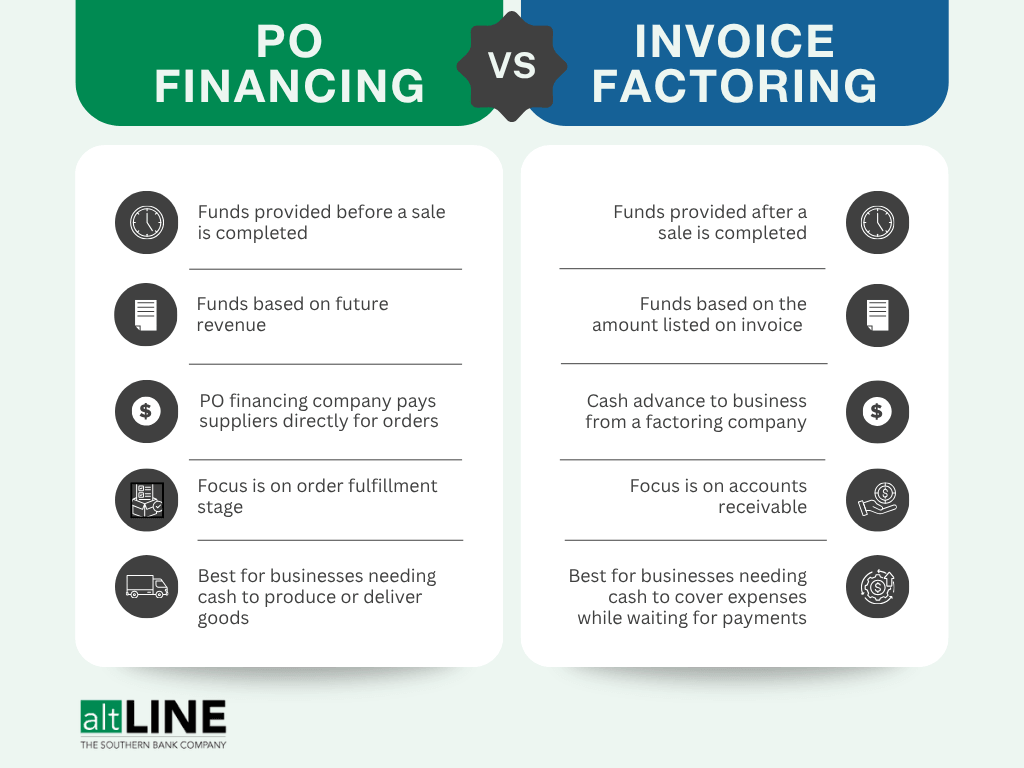

Differences Between Purchase Order (PO) Financing and Factoring

Below is a summary of the key differences between purchase order (PO) financing and invoice factoring.

| Purchase Order (PO) Financing | Invoice Factoring | |

| Purpose | Provides funds before a sale is completed to buy materials or fulfill a customer order. | Provides funds after a sale is completed by advancing cash for unpaid invoices. |

| Funds Based On | The purchase order from a customer (future revenue). | The invoice issued to a customer (completed sale). |

| Who Pays the Lender | The end customer pays the lender directly after the order is fulfilled. | The customer pays the factoring company, which then sends the remaining balance (minus fees) to the business. |

| Best for | Businesses needing cash to produce or deliver goods (e.g., manufacturers, distributors). | Businesses needing cash to cover operating expenses while waiting for payments (e.g., service providers, trucking firms). |

Purchase Order Financing vs. Factoring: Which to Choose?

Both PO financing and invoice factoring come with inherent advantages and disadvantages, and each offers small business owners a specific kind of aid in solving their cash flow problems. Borrowers should consider that company’s specific needs when deciding between purchase order financing or invoice factoring.

A business that needs funds upfront to fulfill an order or begin a project will most likely find that purchase order financing is tailor-made for its purposes. On the other hand, a business that requires needs an instant working capital or cash flow boost, in large part due to long payment terms, will benefit most from invoice factoring

Either way, these forms of financing offer small businesses a more accessible and customizable solution than traditional bank loans.

Jim is the General Manager of altLINE by The Southern Bank. altLINE partners with lenders nationwide to provide invoice factoring and accounts receivable financing to their small and medium-sized business customers. altLINE is a direct bank lender and a division of The Southern Bank Company, a community bank originally founded in 1936.